EDA of SYK

Refer to EDA-UNH for more detailed description for each plot.

Basic Time Series Plot

Show the code

# candlestick plot

SYK_df <- as.data.frame(SYK)

SYK_df$Dates <- as.Date(rownames(SYK_df))

fig_SYK <- SYK_df %>% plot_ly(x = ~Dates, type="candlestick",

open = ~SYK.Open, close = ~SYK.Close,

high = ~SYK.High, low = ~SYK.Low)

fig_SYK <- fig_SYK %>%

layout(title = "Basic Candlestick Chart for Pfizer")

fig_SYKLag plot

Show the code

SYK_ts <- ts(stock_df$SYK, start = c(2010,1),end = c(2023,1),

frequency = 251)

ts_lags(SYK_ts)Decomposed times series

Show the code

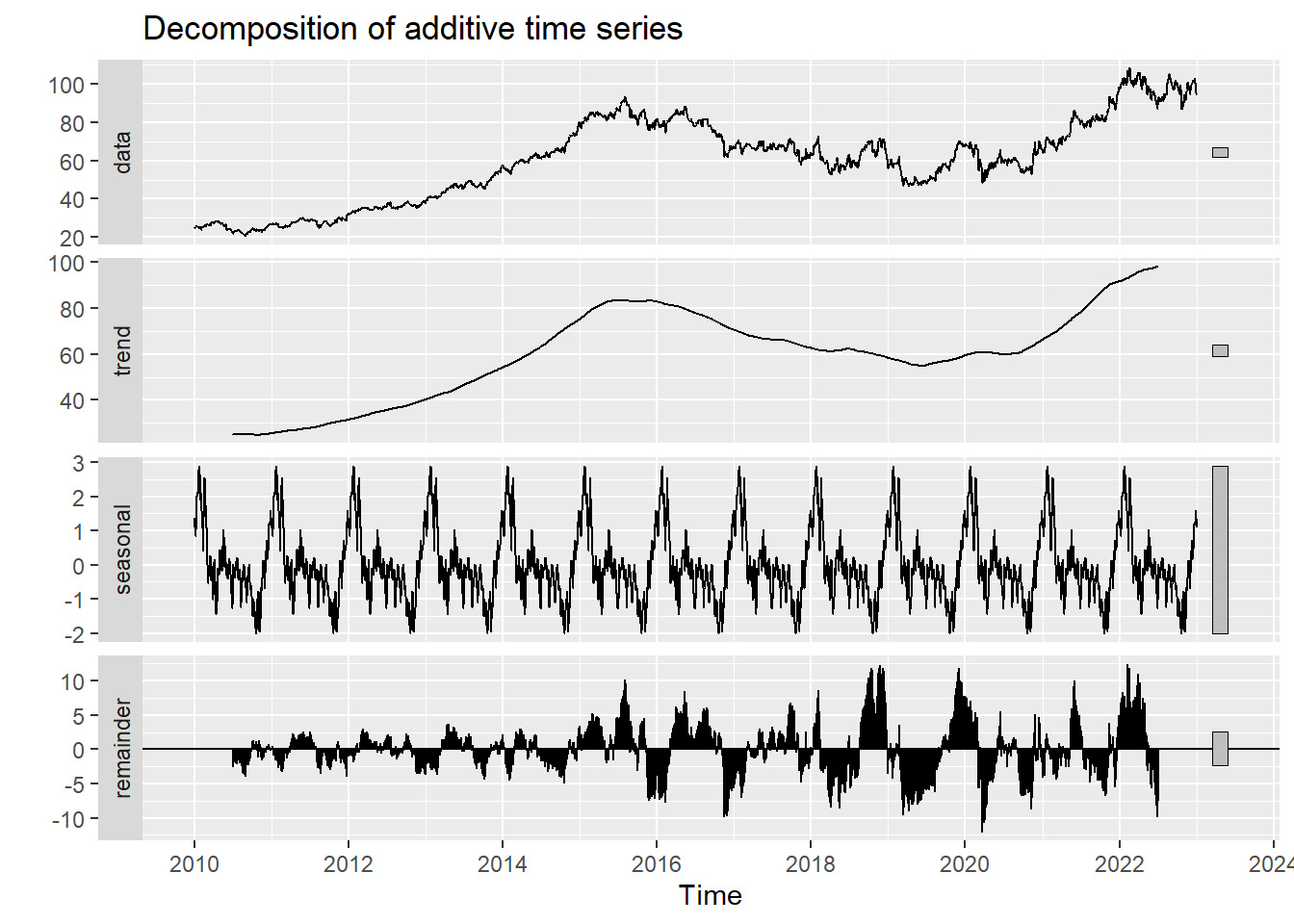

decompose_SYK <- decompose(SYK_ts,'additive')

autoplot(decompose_SYK)

Autocorrelation in Time Series

Show the code

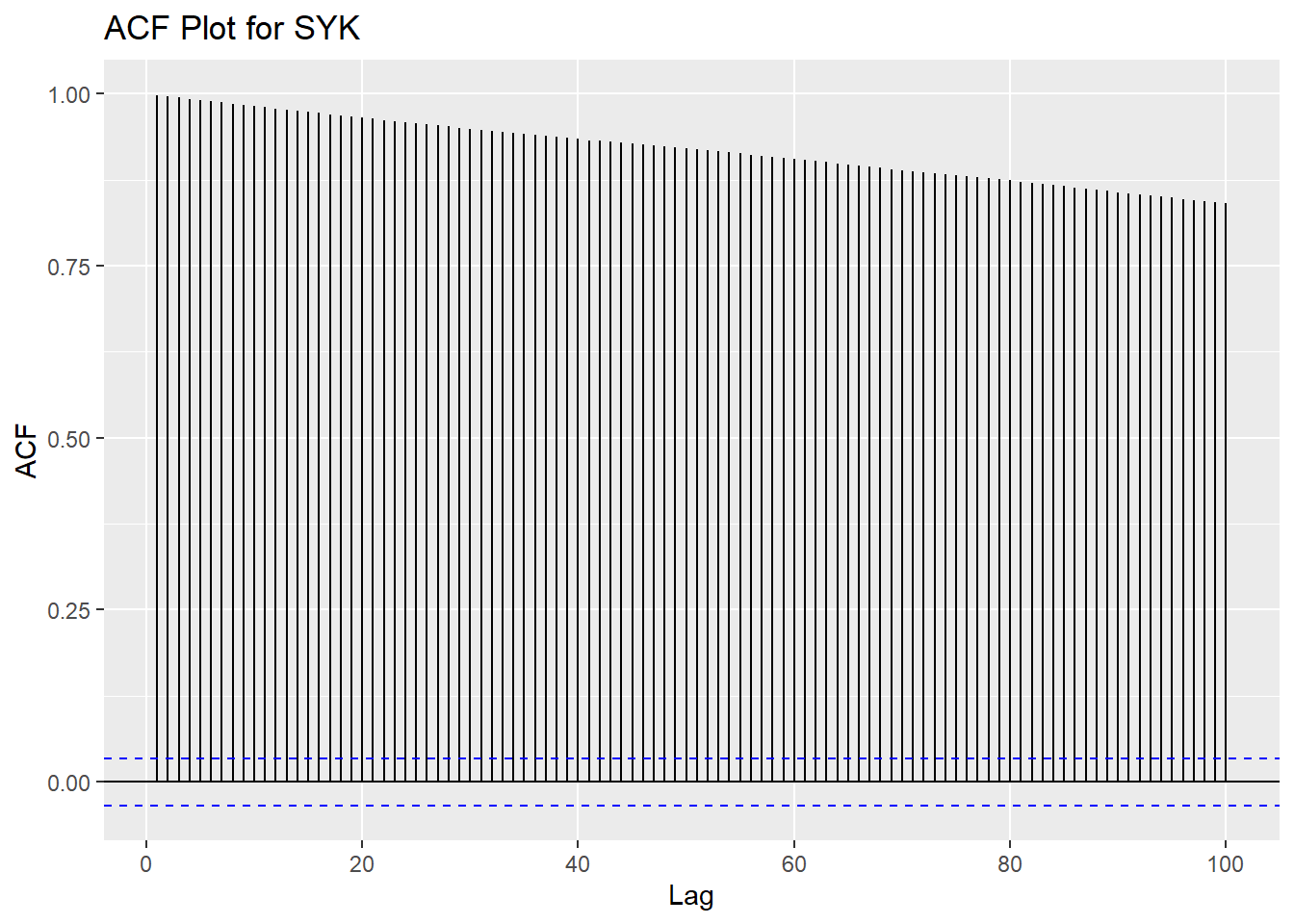

ggAcf(SYK_ts,100)+ggtitle("ACF Plot for SYK")

Show the code

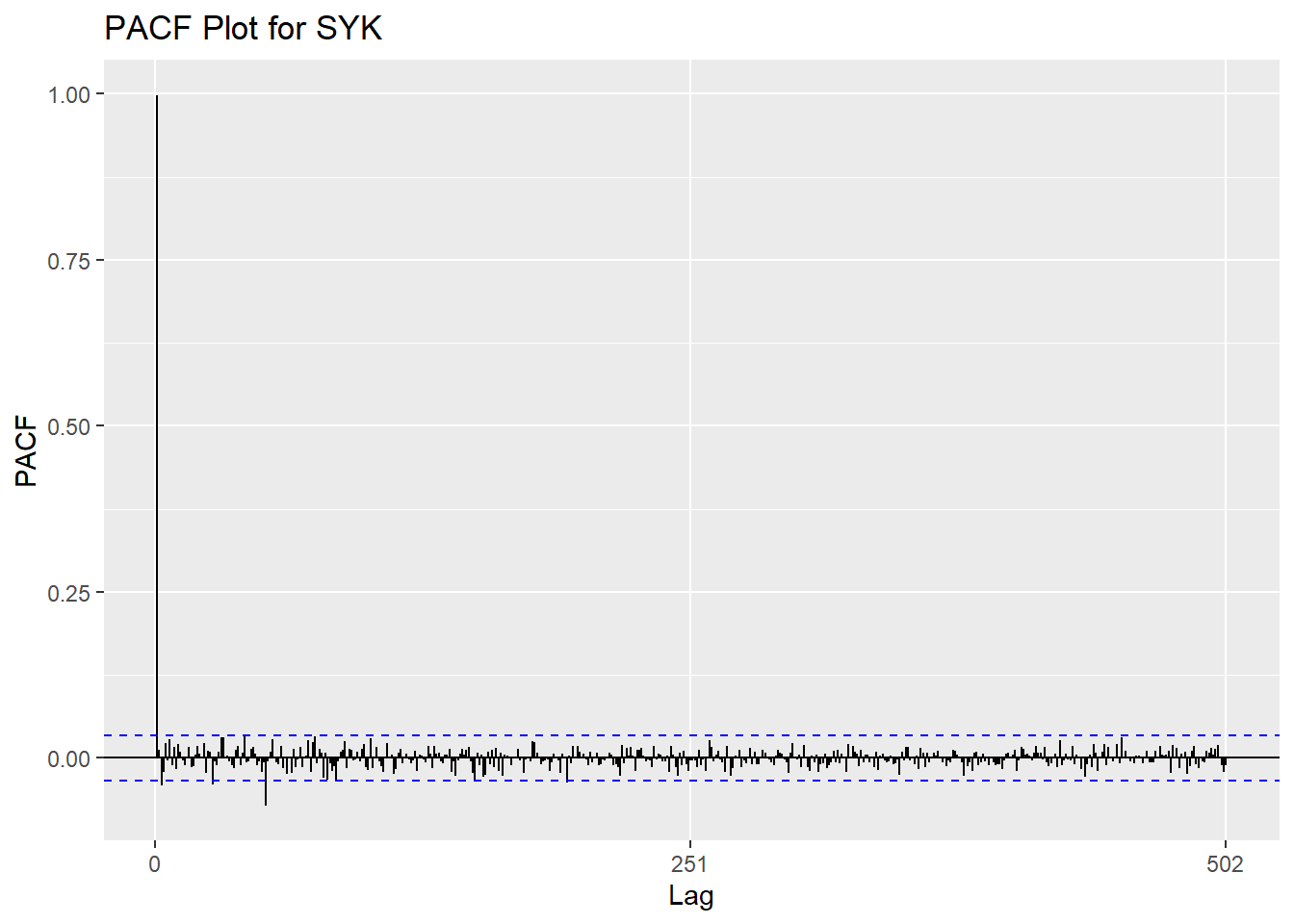

ggPacf(SYK_ts)+ggtitle("PACF Plot for SYK")

Augmented Dickey-Fuller Test

Show the code

tseries::adf.test(SYK_ts)

Augmented Dickey-Fuller Test

data: SYK_ts

Dickey-Fuller = -1.734, Lag order = 14, p-value = 0.6909

alternative hypothesis: stationaryDetrending

Show the code

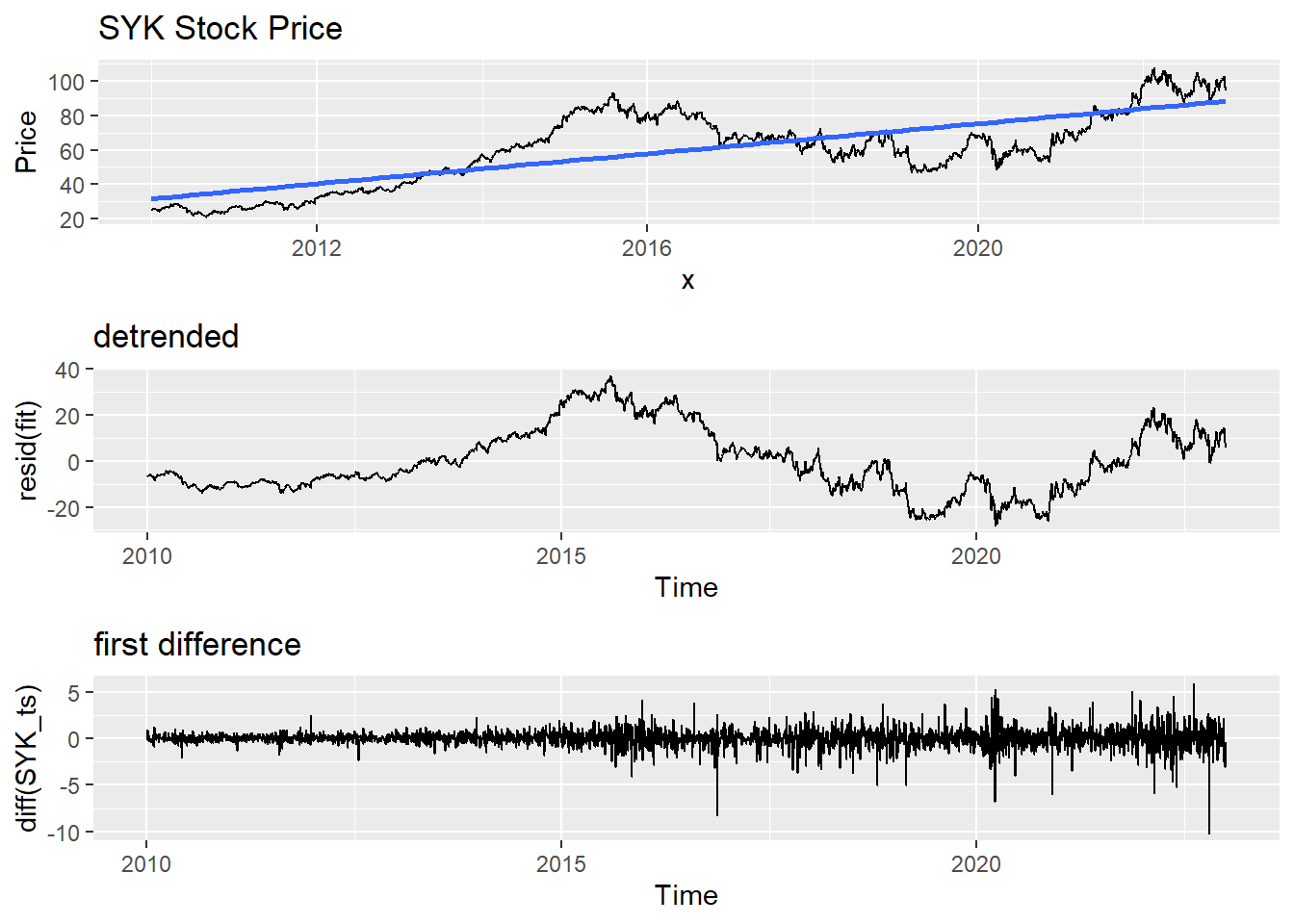

fit = lm(SYK_ts~time(SYK_ts), na.action=NULL)

y= SYK_ts

x=time(SYK_ts)

DD<-data.frame(x,y)

ggp <- ggplot(DD, aes(x, y)) +

geom_line()

ggp <- ggp +

stat_smooth(method = "lm",

formula = y ~ x,

geom = "smooth") +ggtitle("SYK Stock Price")+ylab("Price")

plot1<-autoplot(resid(fit), main="detrended")

plot2<-autoplot(diff(SYK_ts), main="first difference")

grid.arrange(ggp, plot1, plot2,nrow=3)Don't know how to automatically pick scale for object of type <ts>. Defaulting

to continuous.

Don't know how to automatically pick scale for object of type <ts>. Defaulting

to continuous.

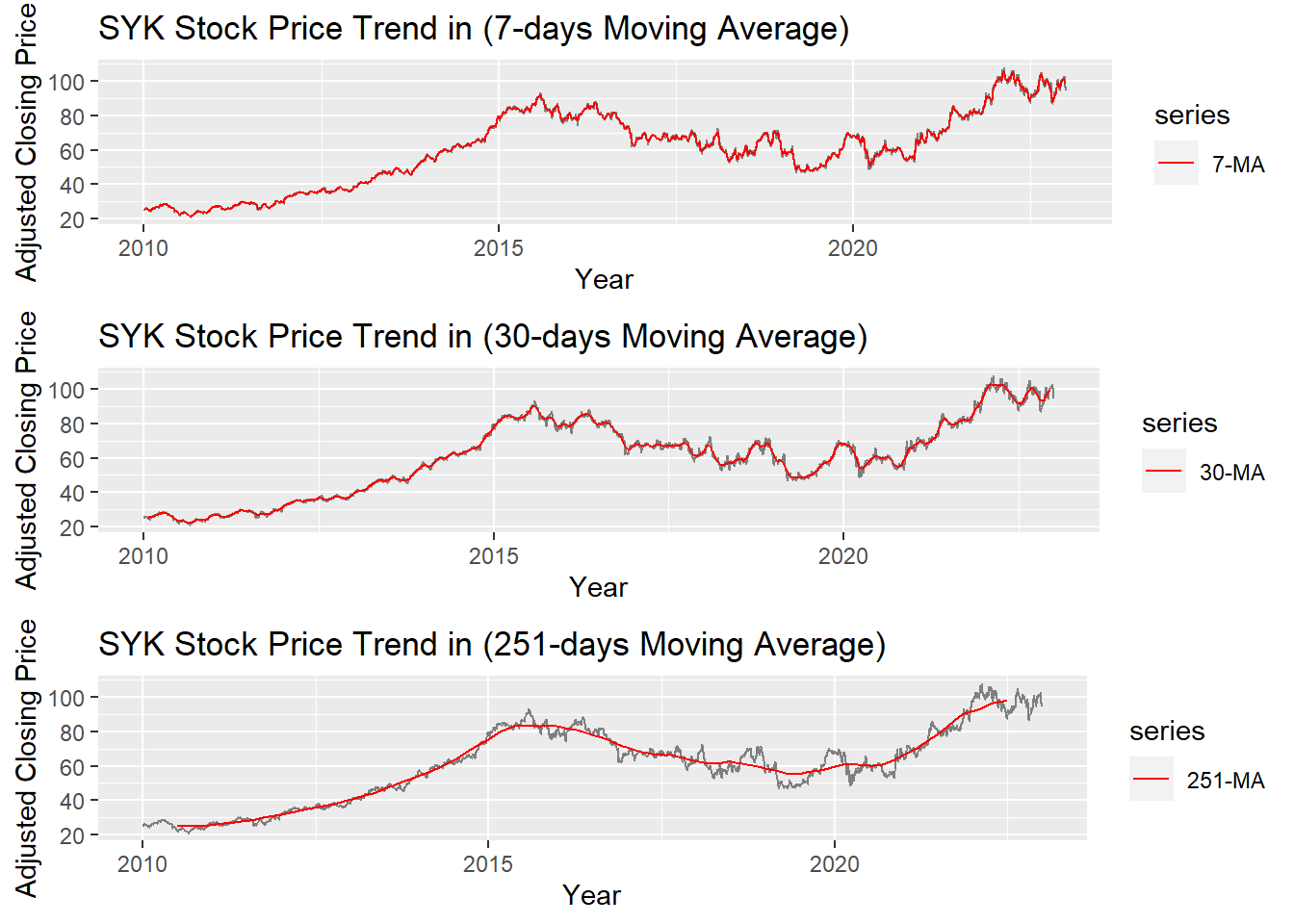

Moving Average Smoothing

Smoothing methods are a family of forecasting methods that average values over multiple periods in order to reduce the noise and uncover patterns in the data. It is useful as a data preparation technique as it can reduce the random variation in the observations and better expose the structure of the underlying causal processes. We call this an m-MA, meaning a moving average of order m.

Show the code

MA_7 <- autoplot(SYK_ts, series="Data") +

autolayer(ma(SYK_ts,7), series="7-MA") +

xlab("Year") + ylab("Adjusted Closing Price") +

ggtitle("SYK Stock Price Trend in (7-days Moving Average)") +

scale_colour_manual(values=c("SYK_ts"="grey50","7-MA"="red"),

breaks=c("SYK_ts","7-MA"))

MA_30 <- autoplot(SYK_ts, series="Data") +

autolayer(ma(SYK_ts,30), series="30-MA") +

xlab("Year") + ylab("Adjusted Closing Price") +

ggtitle("SYK Stock Price Trend in (30-days Moving Average)") +

scale_colour_manual(values=c("SYK_ts"="grey50","30-MA"="red"),

breaks=c("SYK_ts","30-MA"))

MA_251 <- autoplot(SYK_ts, series="Data") +

autolayer(ma(SYK_ts,251), series="251-MA") +

xlab("Year") + ylab("Adjusted Closing Price") +

ggtitle("SYK Stock Price Trend in (251-days Moving Average)") +

scale_colour_manual(values=c("SYK_ts"="grey50","251-MA"="red"),

breaks=c("SYK_ts","251-MA"))

grid.arrange(MA_7, MA_30, MA_251, ncol=1)

The graph above shows the moving average of 7 days, 30 days and 251 days. 251 days was choose because there are around 251 days of stock price data per year. According to the plots, it can be observed that When MA is very large(MA=251), some parts of smoothing line(red) do not fit the real stock price line. While When MA is small(MA=7), the smoothing line(red) fits the real price line. MA-30 greatly fits the real price line. Therefore, MA-30 might be a good parameter for smoothing.