GPD

EDA

Show the code

gdp <- read.csv('data/Employment59.csv')

gdp$DATE <- as.Date(gdp$DATE)

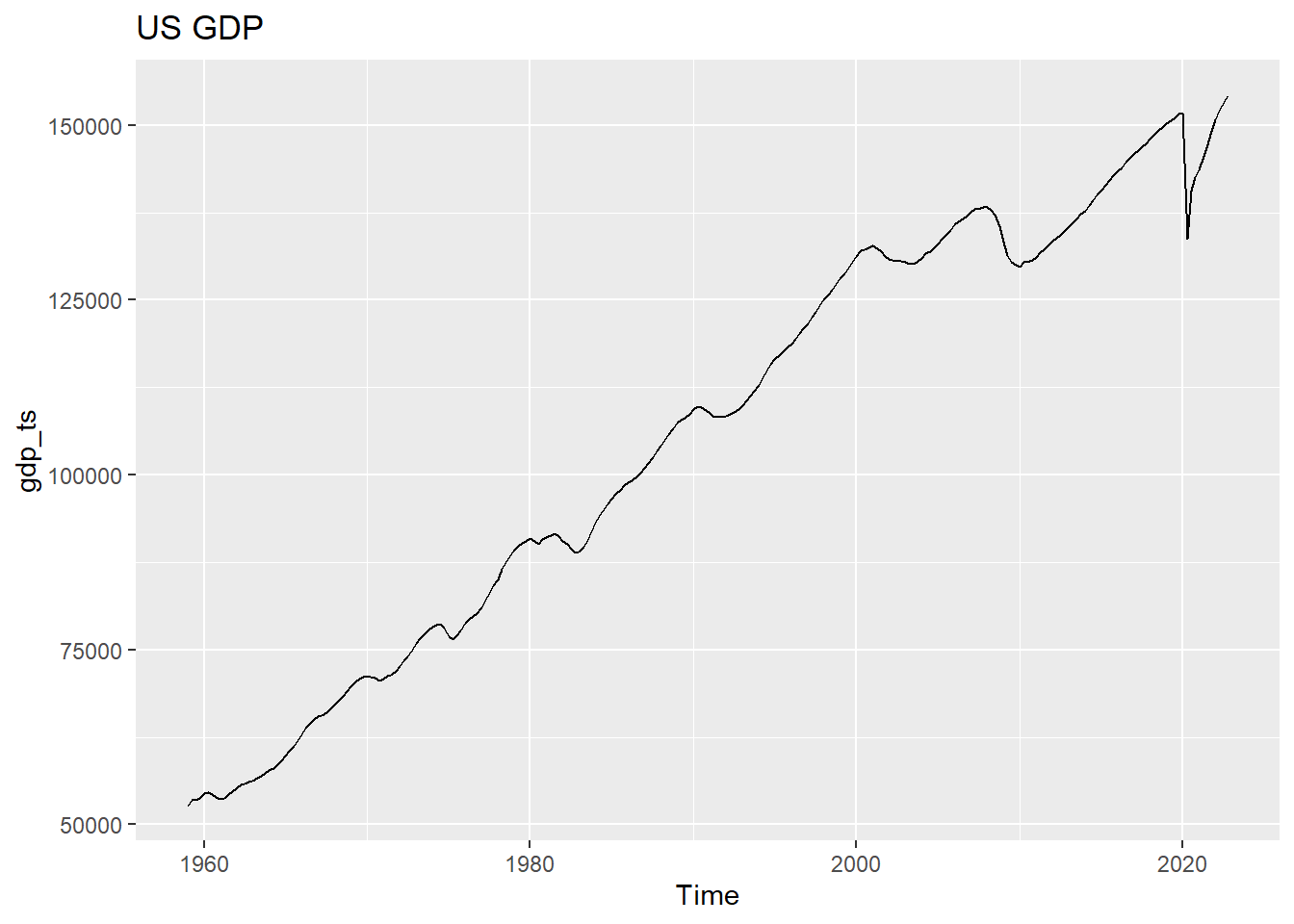

gdp_ts <- ts(gdp$PAYEMS, star= c(1959,1),frequency = 4)

autoplot(gdp_ts)+ggtitle("US GDP")

Show the code

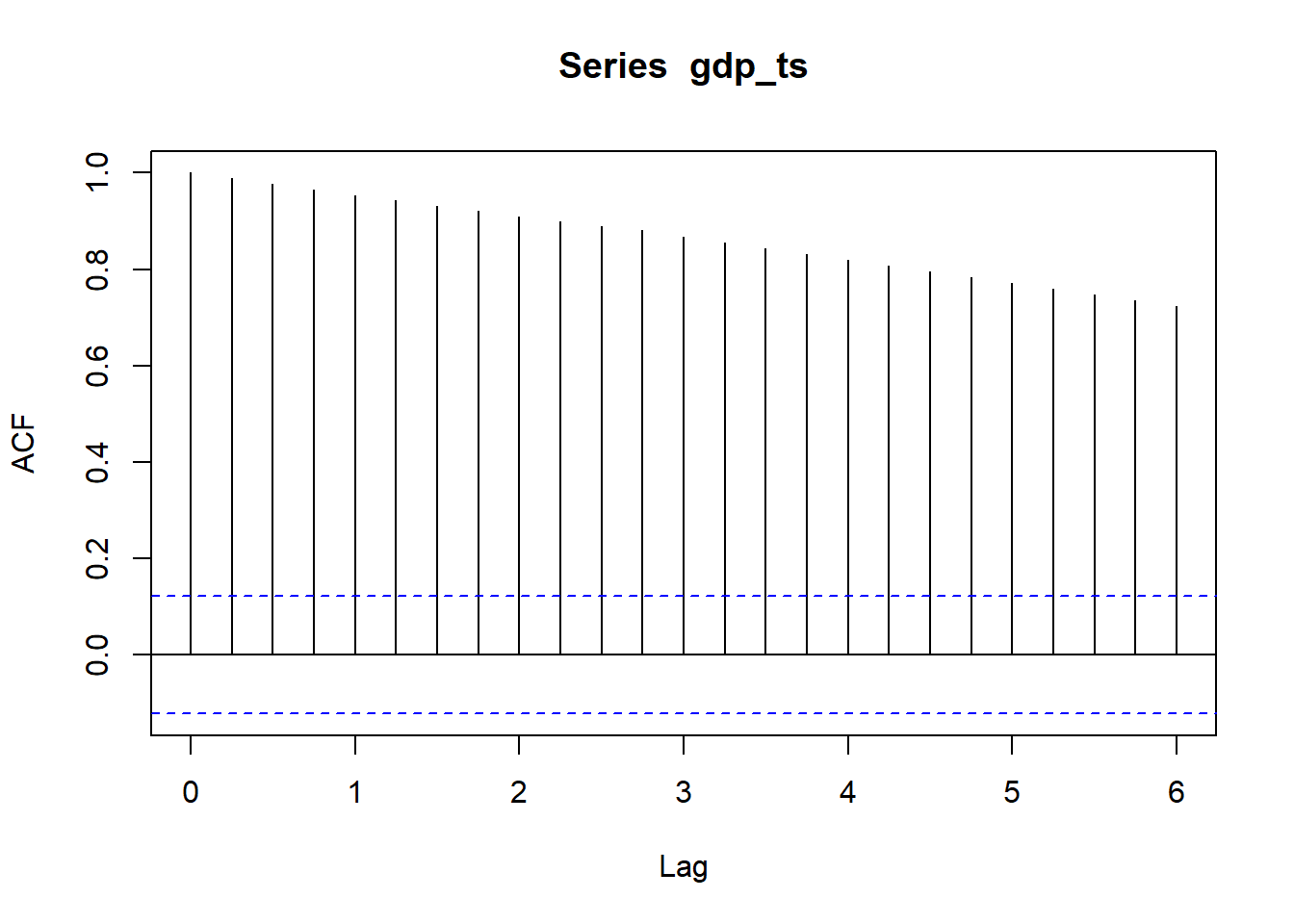

acf(gdp_ts)

Show the code

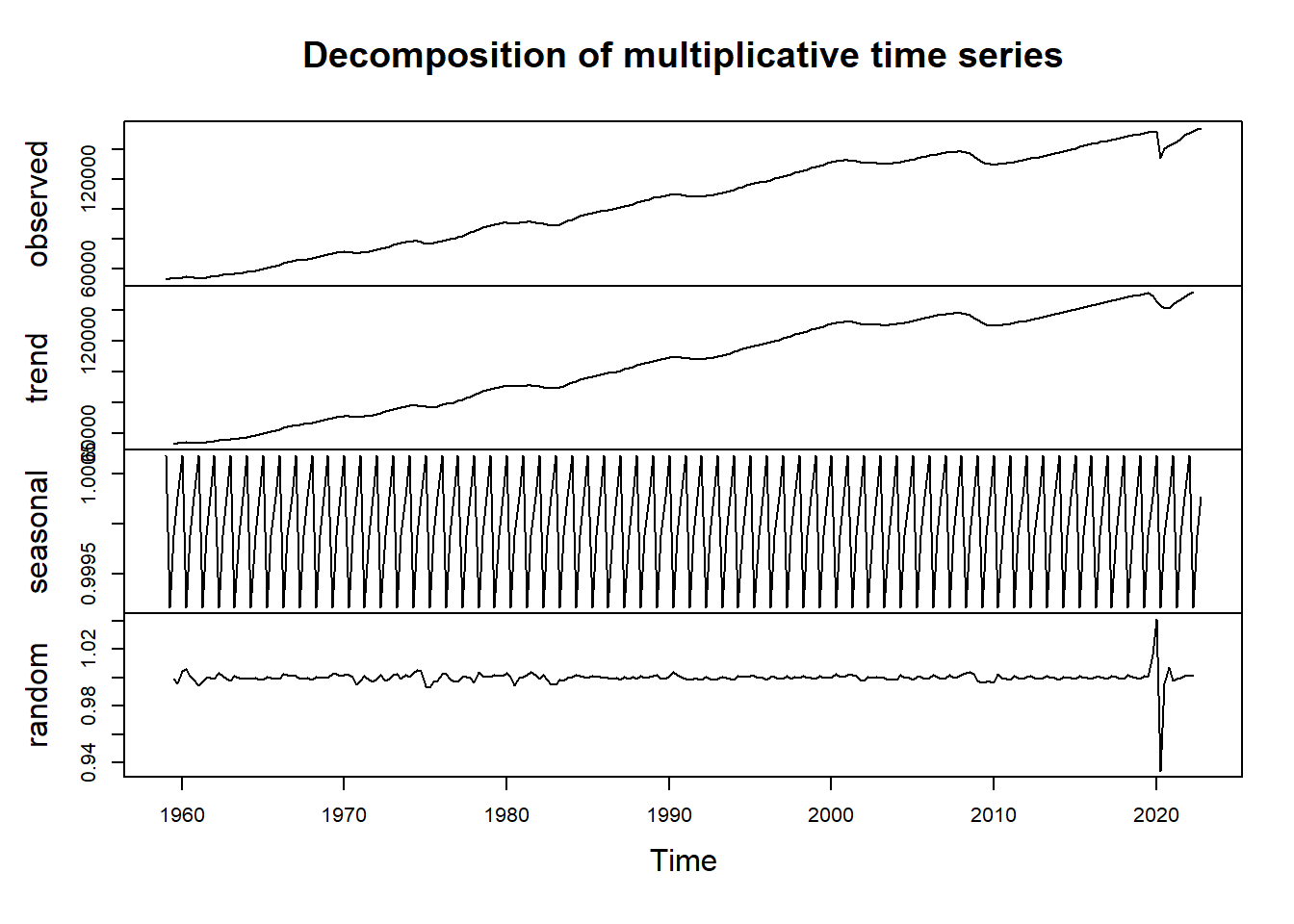

dec2=decompose(gdp_ts,type = "multiplicative")

plot(dec2)

Show the code

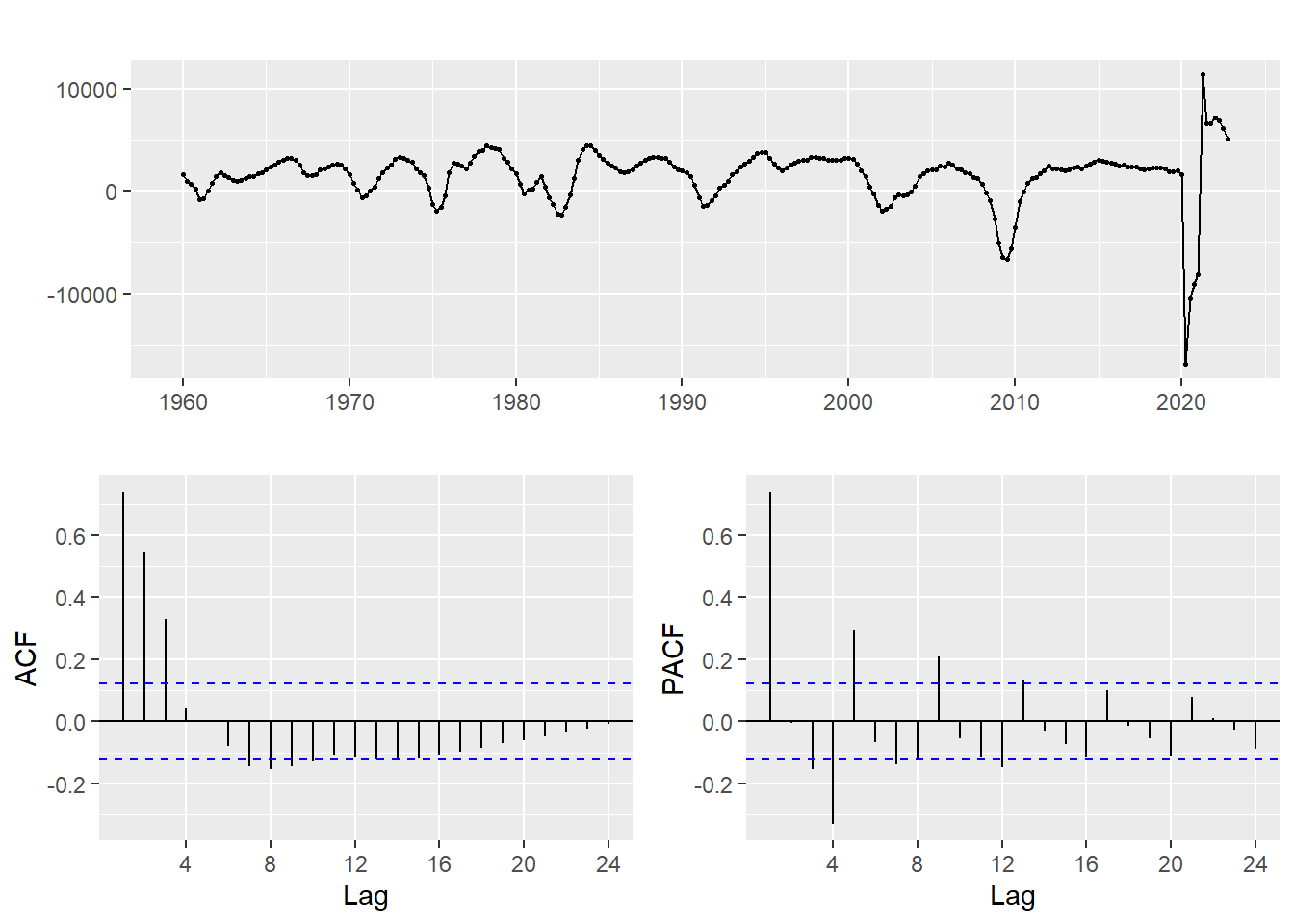

gdp_ts %>% diff() %>% ggtsdisplay() #first ordinary differencing

Show the code

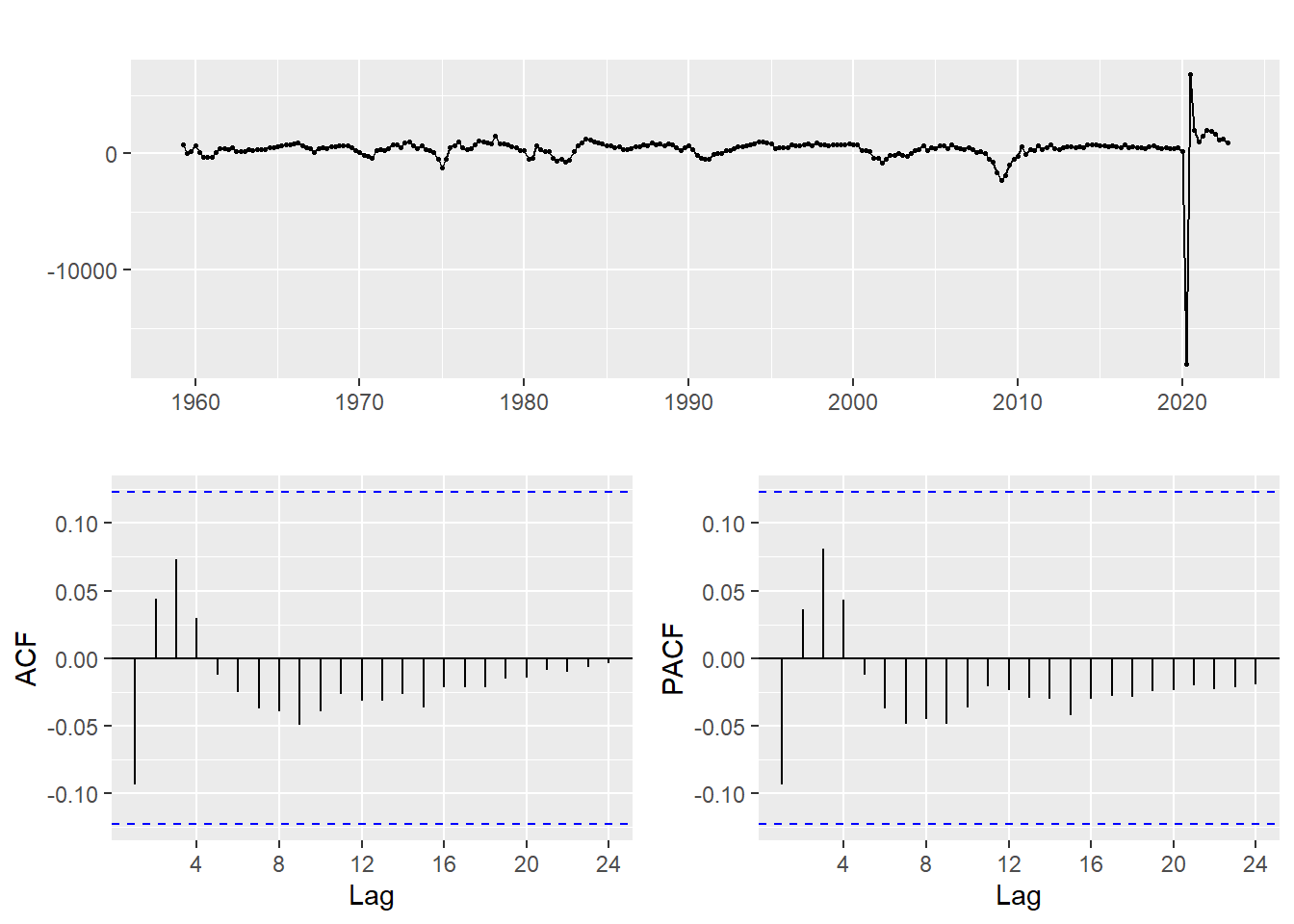

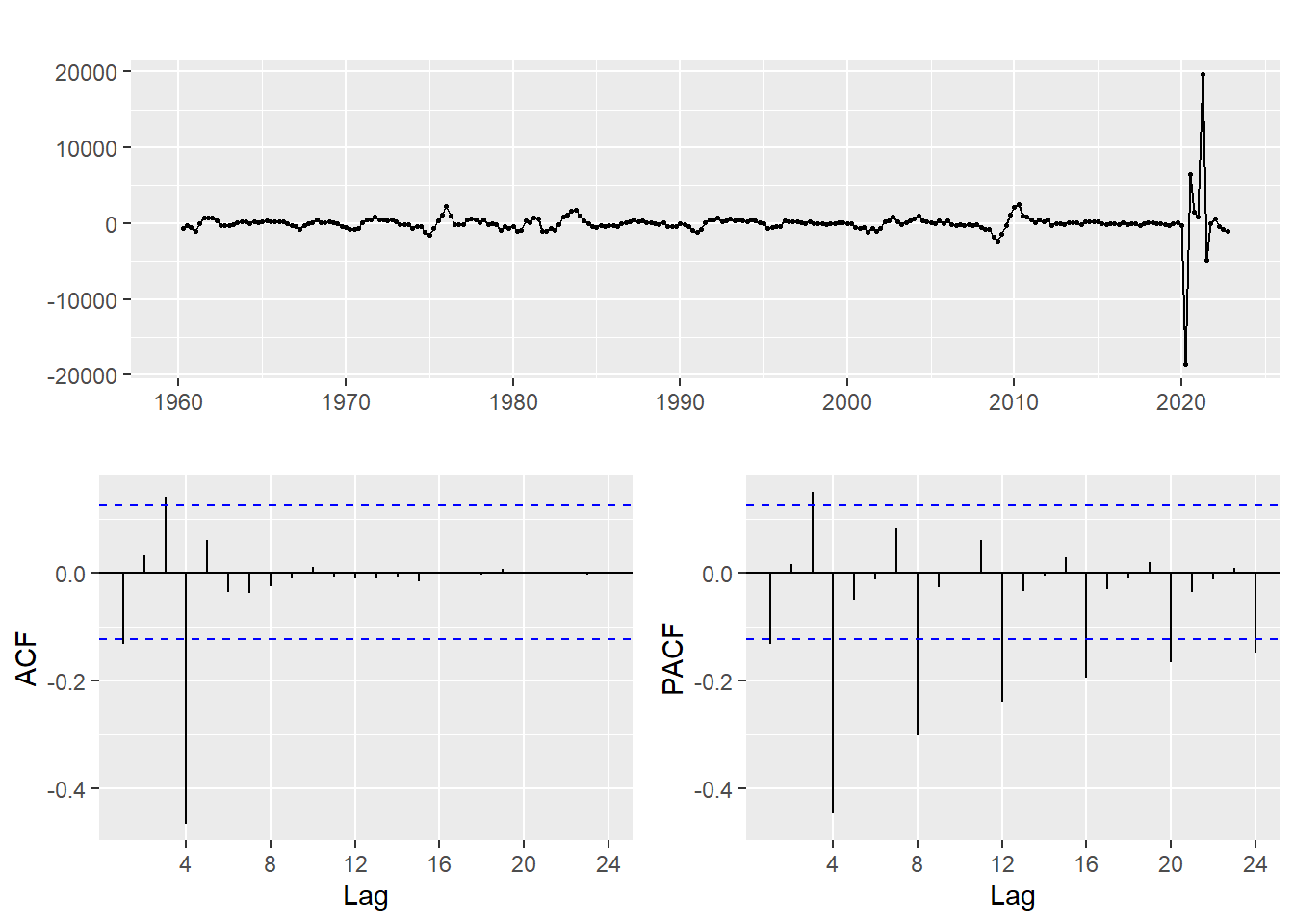

gdp_ts %>% diff(lag = 4) %>% ggtsdisplay() #first ordinary differencing

Determine Parameters

Show the code

gdp_ts %>% diff(lag=4) %>% diff() %>% ggtsdisplay() #do both

p:0,1,3 d:2 q:1,2,3 P:1,2,3 D:2 Q:1

Show the code

######################## Check for different combinations ########

#write a funtion

SARIMA.c=function(p1,p2,q1,q2,P1,P2,Q1,Q2,data){

#K=(p2+1)*(q2+1)*(P2+1)*(Q2+1)

temp=c()

d=1

D=1

s=12

i=1

temp= data.frame()

ls=matrix(rep(NA,9*35),nrow=35)

for (p in p1:p2)

{

for(q in q1:q2)

{

for(P in P1:P2)

{

for(Q in Q1:Q2)

{

if(p+d+q+P+D+Q<=9)

{

model<- Arima(data,order=c(p-1,d,q-1),seasonal=c(P-1,D,Q-1))

ls[i,]= c(p-1,d,q-1,P-1,D,Q-1,model$aic,model$bic,model$aicc)

i=i+1

#print(i)

}

}

}

}

}

temp= as.data.frame(ls)

names(temp)= c("p","d","q","P","D","Q","AIC","BIC","AICc")

temp

}

output = SARIMA.c(p1=1,p2=4,q1=1,q2=4,P1=1,P2=3,Q1=1,Q2=2, data = gdp_ts)

#output

knitr::kable(output)| p | d | q | P | D | Q | AIC | BIC | AICc |

|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 0 | 0 | 1 | 0 | 4498.257 | 4501.782 | 4498.273 |

| 0 | 1 | 0 | 0 | 1 | 1 | 4348.055 | 4355.106 | 4348.104 |

| 0 | 1 | 0 | 1 | 1 | 0 | 4439.336 | 4446.387 | 4439.384 |

| 0 | 1 | 0 | 1 | 1 | 1 | 4350.031 | 4360.607 | 4350.128 |

| 0 | 1 | 0 | 2 | 1 | 0 | 4379.073 | 4389.649 | 4379.170 |

| 0 | 1 | 0 | 2 | 1 | 1 | 4350.737 | 4364.839 | 4350.900 |

| 0 | 1 | 1 | 0 | 1 | 0 | 4496.142 | 4503.193 | 4496.191 |

| 0 | 1 | 1 | 0 | 1 | 1 | 4348.392 | 4358.968 | 4348.489 |

| 0 | 1 | 1 | 1 | 1 | 0 | 4439.612 | 4450.188 | 4439.709 |

| 0 | 1 | 1 | 1 | 1 | 1 | 4350.294 | 4364.396 | 4350.456 |

| 0 | 1 | 1 | 2 | 1 | 0 | 4381.060 | 4395.162 | 4381.223 |

| 0 | 1 | 2 | 0 | 1 | 0 | 4488.150 | 4498.727 | 4488.248 |

| 0 | 1 | 2 | 0 | 1 | 1 | 4349.256 | 4363.357 | 4349.418 |

| 0 | 1 | 2 | 1 | 1 | 0 | 4440.078 | 4454.180 | 4440.241 |

| 0 | 1 | 3 | 0 | 1 | 0 | 4478.378 | 4492.480 | 4478.541 |

| 1 | 1 | 0 | 0 | 1 | 0 | 4495.859 | 4502.910 | 4495.907 |

| 1 | 1 | 0 | 0 | 1 | 1 | 4348.206 | 4358.782 | 4348.303 |

| 1 | 1 | 0 | 1 | 1 | 0 | 4439.428 | 4450.005 | 4439.525 |

| 1 | 1 | 0 | 1 | 1 | 1 | 4350.101 | 4364.203 | 4350.264 |

| 1 | 1 | 0 | 2 | 1 | 0 | 4381.057 | 4395.159 | 4381.220 |

| 1 | 1 | 1 | 0 | 1 | 0 | 4497.843 | 4508.419 | 4497.940 |

| 1 | 1 | 1 | 0 | 1 | 1 | 4350.038 | 4364.139 | 4350.200 |

| 1 | 1 | 1 | 1 | 1 | 0 | 4441.326 | 4455.428 | 4441.489 |

| 1 | 1 | 2 | 0 | 1 | 0 | 4489.217 | 4503.319 | 4489.380 |

| 2 | 1 | 0 | 0 | 1 | 0 | 4497.803 | 4508.379 | 4497.900 |

| 2 | 1 | 0 | 0 | 1 | 1 | 4349.683 | 4363.785 | 4349.845 |

| 2 | 1 | 0 | 1 | 1 | 0 | 4441.003 | 4455.105 | 4441.165 |

| 2 | 1 | 1 | 0 | 1 | 0 | 4499.678 | 4513.780 | 4499.841 |

| 3 | 1 | 0 | 0 | 1 | 0 | 4494.238 | 4508.340 | 4494.400 |

| NA | NA | NA | NA | NA | NA | NA | NA | NA |

| NA | NA | NA | NA | NA | NA | NA | NA | NA |

| NA | NA | NA | NA | NA | NA | NA | NA | NA |

| NA | NA | NA | NA | NA | NA | NA | NA | NA |

| NA | NA | NA | NA | NA | NA | NA | NA | NA |

| NA | NA | NA | NA | NA | NA | NA | NA | NA |

Show the code

output[which.min(output$AIC),] p d q P D Q AIC BIC AICc

2 0 1 0 0 1 1 4348.055 4355.106 4348.104Show the code

output[which.min(output$BIC),] p d q P D Q AIC BIC AICc

2 0 1 0 0 1 1 4348.055 4355.106 4348.104Show the code

output[which.min(output$AICc),] p d q P D Q AIC BIC AICc

2 0 1 0 0 1 1 4348.055 4355.106 4348.104Show the code

set.seed(123)

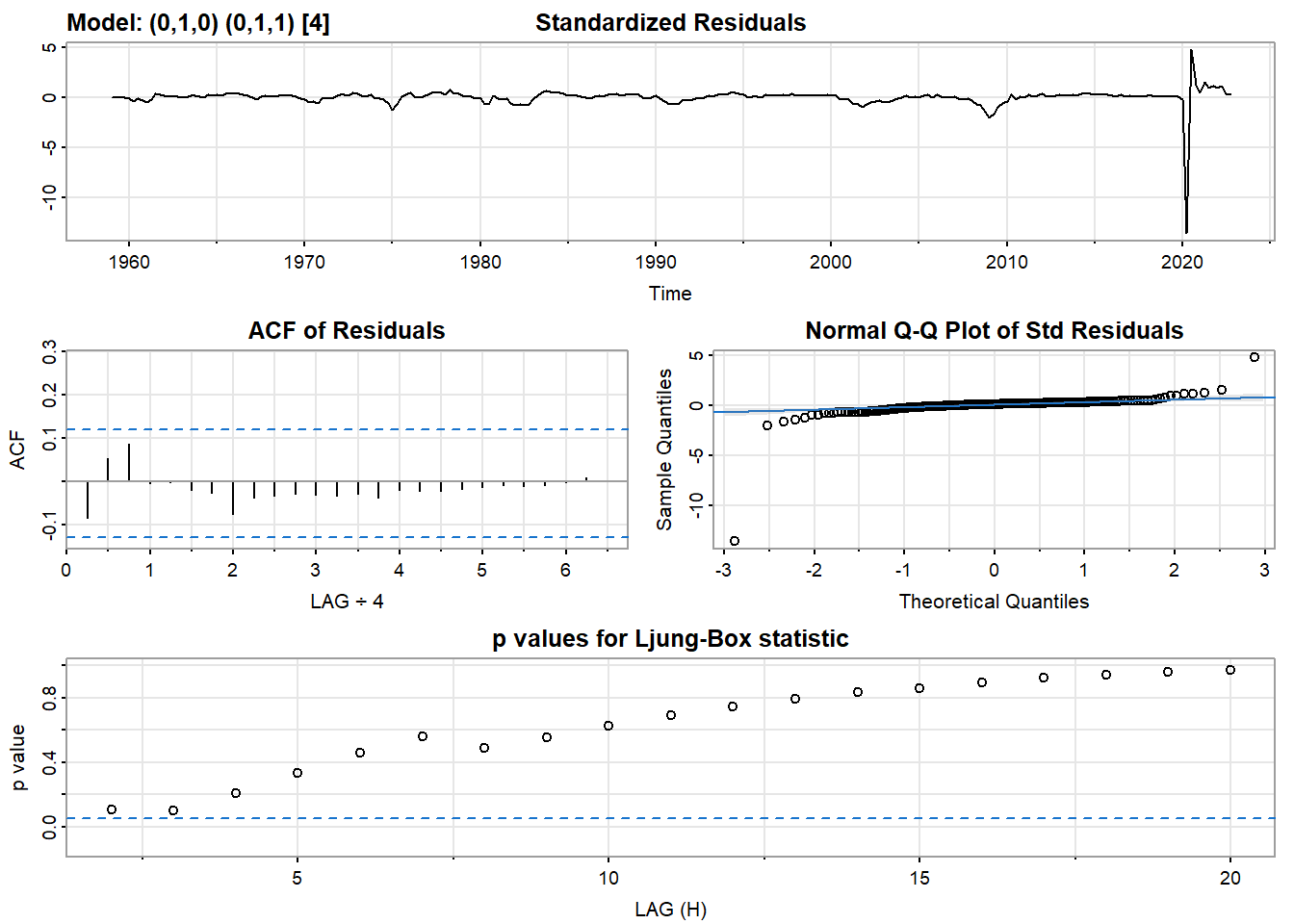

model_output <- capture.output(sarima(gdp_ts, 0,1,0,0,1,1,4))

Show the code

cat(model_output[21:50], model_output[length(model_output)], sep = "\n")$fit

Call:

arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D, Q), period = S),

include.mean = !no.constant, transform.pars = trans, fixed = fixed, optim.control = list(trace = trc,

REPORT = 1, reltol = tol))

Coefficients:

sma1

-0.9492

s.e. 0.0345

sigma^2 estimated as 1852941: log likelihood = -2172.03, aic = 4348.06

$degrees_of_freedom

[1] 250

$ttable

Estimate SE t.value p.value

sma1 -0.9492 0.0345 -27.4916 0

$AIC

[1] 17.32293

$AICc

[1] 17.32299

$BIC

[1] 17.35102Model Fitting

Show the code

fit <- Arima(gdp_ts, order=c(0,1,0), seasonal=c(0,1,1))

summary(fit)Series: gdp_ts

ARIMA(0,1,0)(0,1,1)[4]

Coefficients:

sma1

-0.9492

s.e. 0.0345

sigma^2 = 1860405: log likelihood = -2172.03

AIC=4348.06 AICc=4348.1 BIC=4355.11

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set 3.482494 1347.888 492.0962 0.0137906 0.4616182 0.2031885

ACF1

Training set -0.08526289forecasting

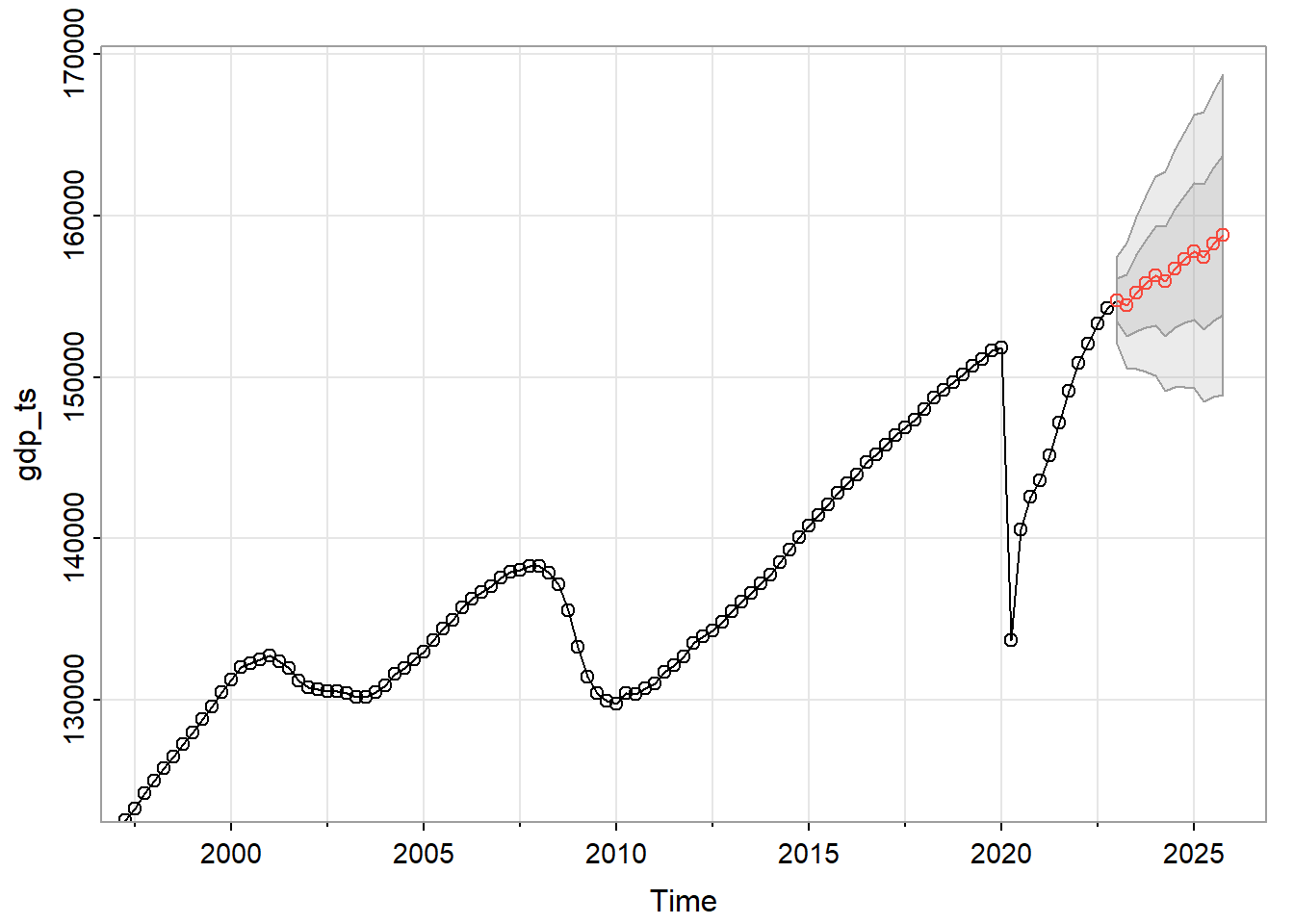

Show the code

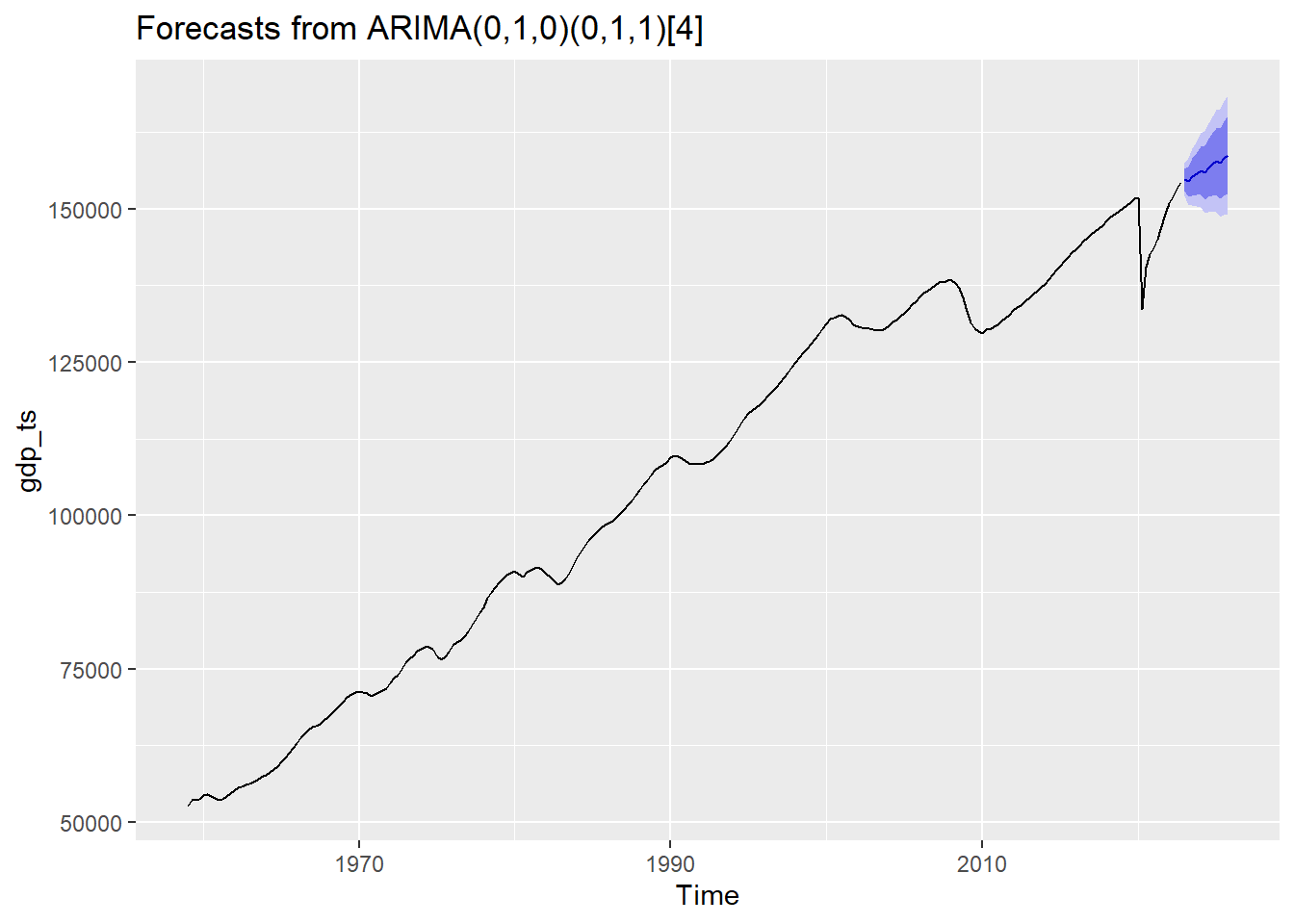

fit %>% forecast(h=12) %>% autoplot() #next 3 years

Show the code

sarima.for(gdp_ts, 12, 0,1,0,0,1,1,4)

$pred

Qtr1 Qtr2 Qtr3 Qtr4

2023 154768.4 154437.3 155221.5 155790.7

2024 156273.1 155942.0 156726.2 157295.5

2025 157777.8 157446.7 158231.0 158800.2

$se

Qtr1 Qtr2 Qtr3 Qtr4

2023 1361.322 1925.194 2357.869 2722.631

2024 3075.622 3392.066 3681.408 3949.611

2025 4224.838 4483.186 4727.437 4959.674Compare with Benchmark methods

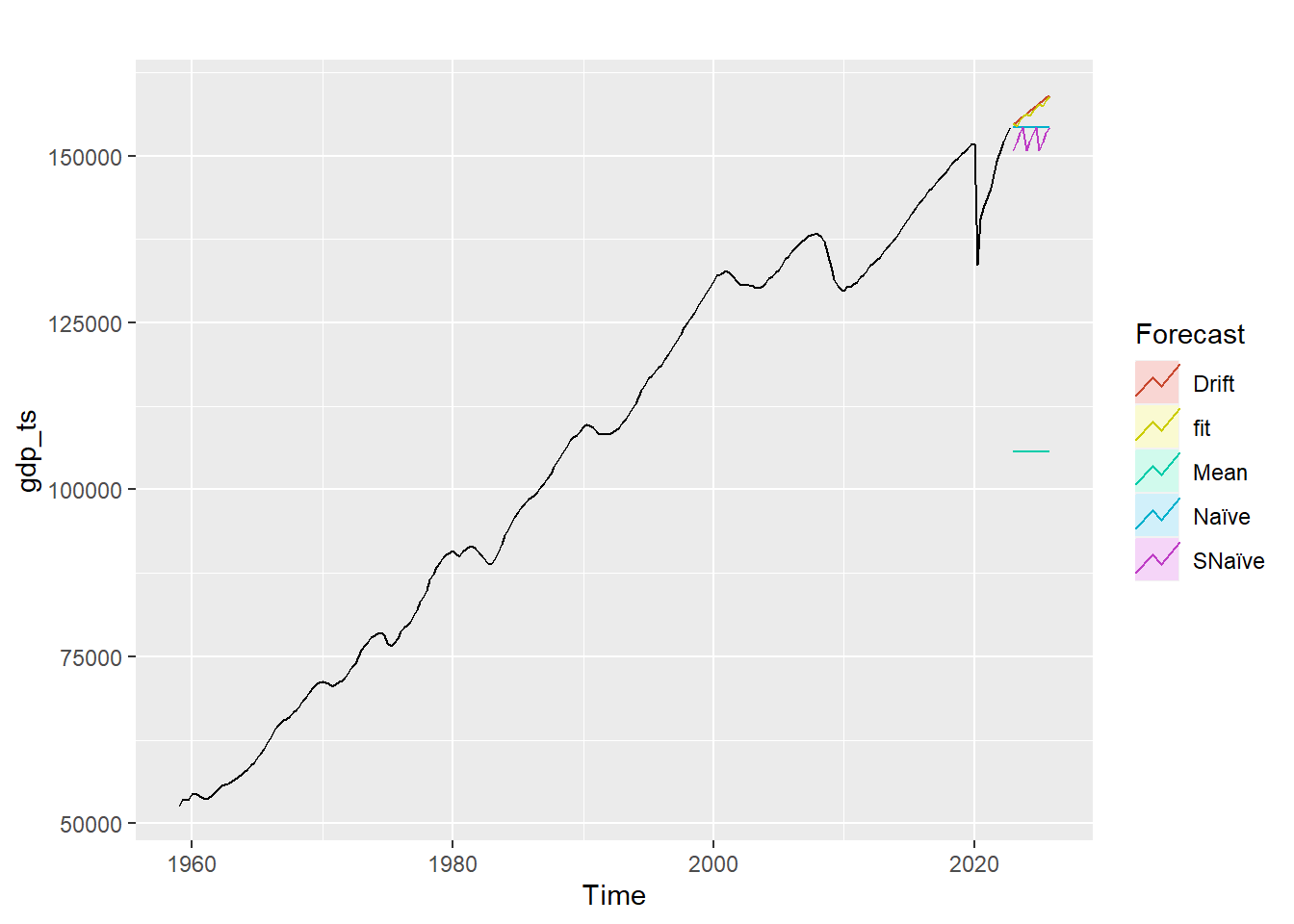

Show the code

fit <- Arima(gdp_ts, order=c(0,1,0), seasonal=c(0,1,1))

autoplot(gdp_ts) +

autolayer(meanf(gdp_ts, h=12),

series="Mean", PI=FALSE) +

autolayer(naive(gdp_ts, h=12),

series="Naïve", PI=FALSE) +

autolayer(snaive(gdp_ts, h=12),

series="SNaïve", PI=FALSE)+

autolayer(rwf(gdp_ts, h=12, drift=TRUE),

series="Drift", PI=FALSE)+

autolayer(forecast(fit,12),

series="fit",PI=FALSE) +

guides(colour=guide_legend(title="Forecast"))

Show the code

f2 <- snaive(gdp_ts, h=12)

accuracy(f2) ME RMSE MAE MPE MAPE MASE ACF1

Training set 1575.474 3048.225 2421.87 1.628746 2.330202 1 0.7384914Show the code

summary(fit)Series: gdp_ts

ARIMA(0,1,0)(0,1,1)[4]

Coefficients:

sma1

-0.9492

s.e. 0.0345

sigma^2 = 1860405: log likelihood = -2172.03

AIC=4348.06 AICc=4348.1 BIC=4355.11

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set 3.482494 1347.888 492.0962 0.0137906 0.4616182 0.2031885

ACF1

Training set -0.08526289Cross Validation

Show the code

k <- 75 # minimum data length for fitting a model n*0.3

n <- length(gdp_ts)

i=1

err1 = c()

#err2 = c()

for(i in 1:(n-k))

{

xtrain <- gdp_ts[1:(k-1)+i] #observations from 1 to 75

xtest <- gdp_ts[k+i] #76th observation as the test set

# Arima(gdp_ts, order=c(0,1,0), seasonal=c(0,1,1))

fit <- Arima(xtrain, order=c(0,1,0), seasonal=c(0,1,1),include.drift=FALSE, method="ML")

fcast1 <- forecast(fit, h=1)

#capture error for each iteration

# This is mean absolute error

err1 = c(err1, abs(fcast1$mean-xtest))

#err2 = c(err2, abs(fcast2$mean-xtest))

# This is mean squared error

err3 = c(err1, (fcast1$mean-xtest)^2)

#err4 = c(err2, (fcast2$mean-xtest)^2)

}

(MAE1=mean(err1)) # This is mean absolute error[1] 771.8619Show the code

MSE1=mean(err1)

MSE1[1] 771.8619