ARMA/ARIMA/SARIMA Models for LLY

Step 1: Determine the stationality of time series

Stationality is a pre-requirement of training ARIMA model. This is because term ‘Auto Regressive’ in ARIMA means it is a linear regression model that uses its own lags as predictors, which work best when the predictors are not correlated and are independent of each other. Stationary time series make sure the statistical properties of time series do not change over time.

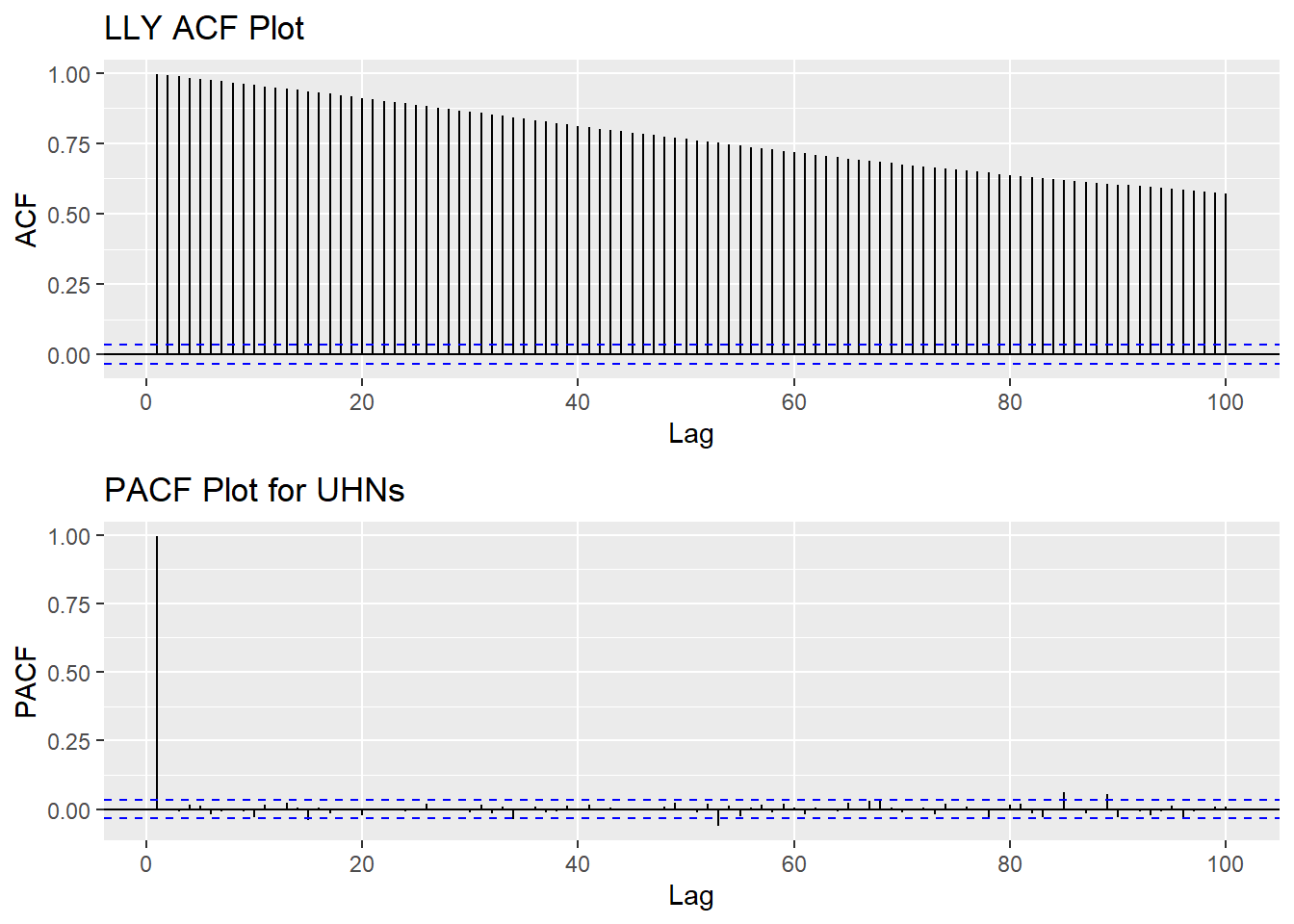

Based on information obtained from both ACF graphs and Augmented Dickey-Fuller Test, the time series data is non-stationary.

Show the code

LLY_acf <- ggAcf(LLY_ts,100)+ggtitle("LLY ACF Plot")

LLY_pacf <- ggPacf(LLY_ts,100)+ggtitle("PACF Plot for UHNs")

grid.arrange(LLY_acf, LLY_pacf,nrow=2)

Show the code

tseries::adf.test(LLY_ts)

Augmented Dickey-Fuller Test

data: LLY_ts

Dickey-Fuller = -2.8006, Lag order = 14, p-value = 0.2393

alternative hypothesis: stationaryStep 2: Eliminate Non-Stationality

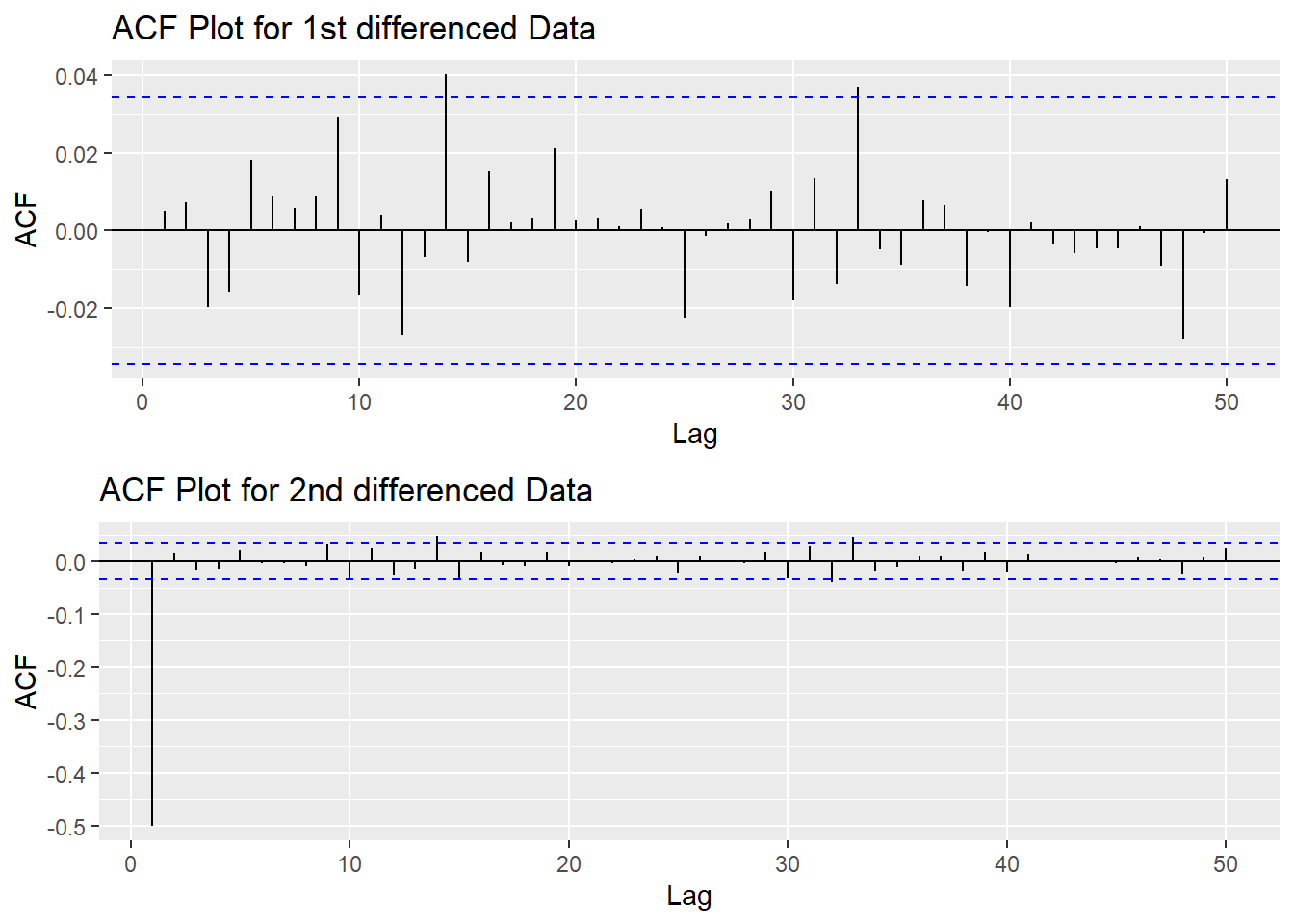

Since this data is non-stationary, it is important to necessary to convert it to stationary time series. This step employs a series of actions to eliminate non-stationality, i.e. differencing the data. It turns out the 1st differened data has shown good stationary property, there are no need to go further at 2nd differencing. What is more, the Augmented Dickey-Fuller Test also confirmed that the 1st differenced data is stationary. Therefore, the1st differencing would be the actions taken to eliminate the non-stationality.

Show the code

plot1<- ggAcf((LLY_ts) %>%diff(), 50, main="ACF Plot for 1st differenced Data")

plot2<- ggAcf((LLY_ts) %>%diff()%>%diff(),50, main="ACF Plot for 2nd differenced Data")

grid.arrange(plot1, plot2,nrow=2)

Show the code

tseries::adf.test((LLY_ts) %>%diff())

Augmented Dickey-Fuller Test

data: (LLY_ts) %>% diff()

Dickey-Fuller = -14.381, Lag order = 14, p-value = 0.01

alternative hypothesis: stationaryStep 3: Determine p,d,q Parameters

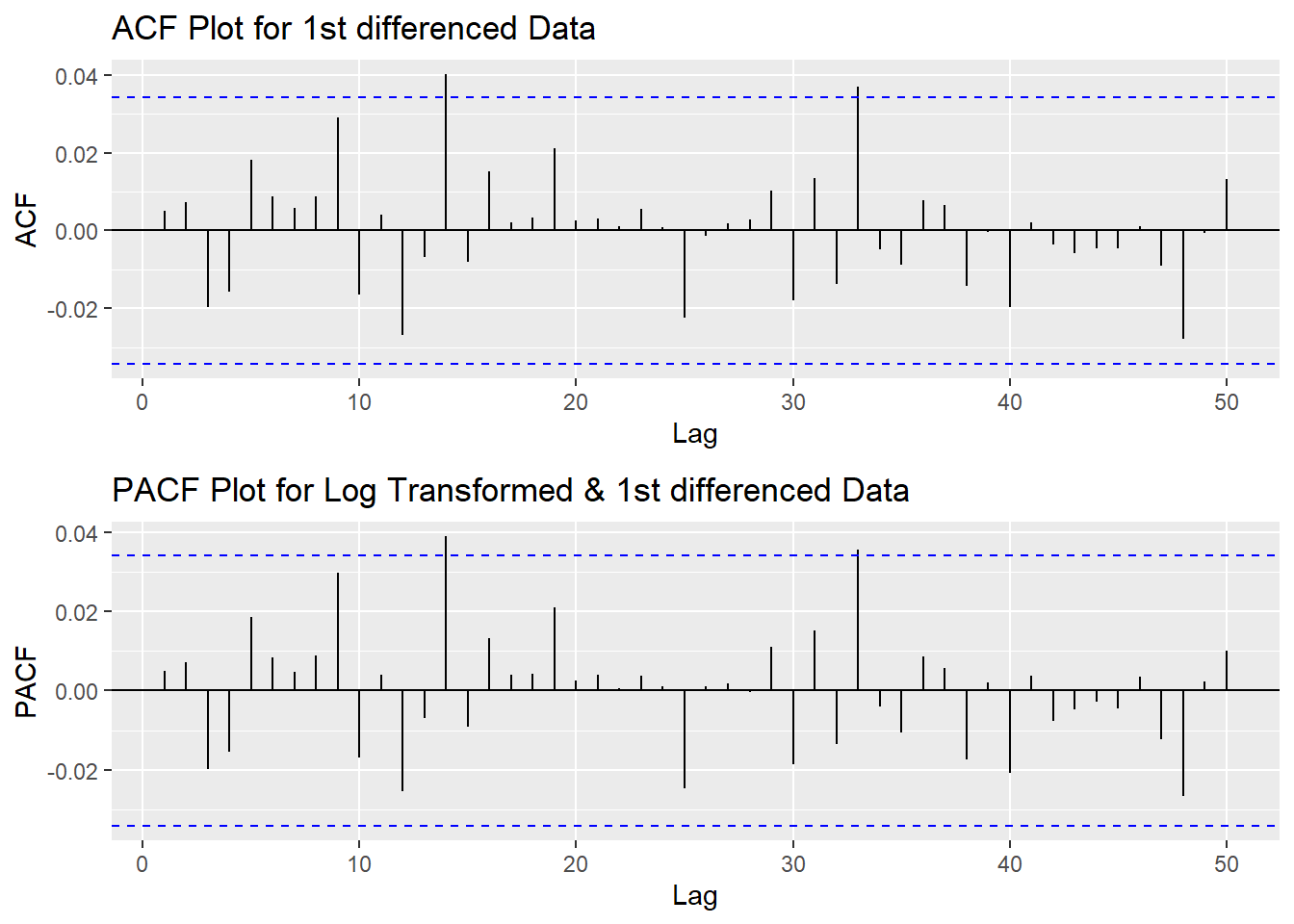

The standard notation of ARIMA(p,d,q) include p,d,q 3 parameters. Here are the representations: - p: The number of lag observations included in the model, also called the lag order; order of the AR term. - d: The number of times that the raw observations are differenced, also called the degree of differencing; number of differencing required to make the time series stationary. - q: order of moving average; order of the MA term. It refers to the number of lagged forecast errors that should go into the ARIMA Model.

Show the code

plot3<- ggPacf((LLY_ts) %>%diff(),50, main="PACF Plot for Log Transformed & 1st differenced Data")

grid.arrange(plot1,plot3)

According to the PACF plot and ACF plot above, there are no significant peaks on both graph, therefore, here set both p and q as 0. Since I only differenced the data once, the d would be 1.

Step 4: Fit ARIMA(p,d,q) model

Show the code

fit1 <- Arima((LLY_ts), order=c(0, 1, 0),include.drift = TRUE)

summary(fit1)Series: (LLY_ts)

ARIMA(0,1,0) with drift

Coefficients:

drift

0.0183

s.e. 0.1283

sigma^2 = 53.71: log likelihood = -11128.73

AIC=22261.47 AICc=22261.47 BIC=22273.65

Training set error measures:

ME RMSE MAE MPE MAPE MASE

Training set 2.349624e-05 7.326456 2.206738 -0.1331229 1.443189 0.02767164

ACF1

Training set 0.004971149Model Diagnostics

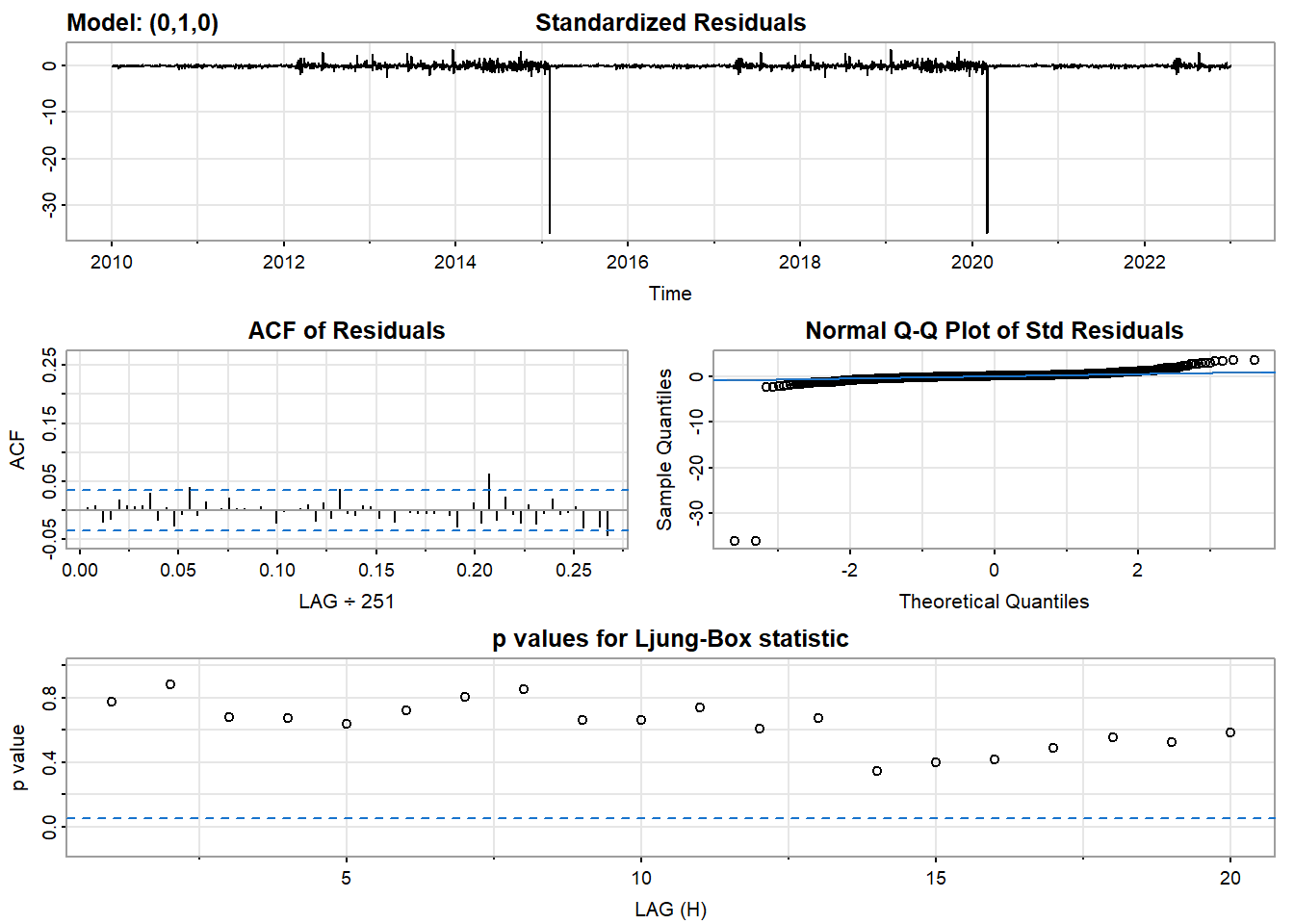

- Inspection of the time plot of the standardized residuals below shows no obvious patterns.

- Notice that there may be outliers, with a few values exceeding 3 standard deviations in magnitude.

- The ACF of the standardized residuals shows no apparent departure from the model assumptions, no significant lags shown.

- The normal Q-Q plot of the residuals shows that the assumption of normality is reasonable, with the exception of the fat-tailed.

- The model appears to fit well.

Show the code

model_output <- capture.output(sarima((LLY_ts), 0,1,0))

Show the code

cat(model_output[9:37], model_output[length(model_output)], sep = "\n") #to get rid of the convergence status and details of the optimization algorithm used by the sarima() $fit

Call:

arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D, Q), period = S),

xreg = constant, transform.pars = trans, fixed = fixed, optim.control = list(trace = trc,

REPORT = 1, reltol = tol))

Coefficients:

constant

0.0183

s.e. 0.1283

sigma^2 estimated as 53.69: log likelihood = -11128.73, aic = 22261.47

$degrees_of_freedom

[1] 3262

$ttable

Estimate SE t.value p.value

constant 0.0183 0.1283 0.143 0.8863

$AIC

[1] 6.822393

$AICc

[1] 6.822394

$BIC

[1] 6.826126Compare with auto.arima() function

auto.arima() returns best ARIMA model according to either AIC, AICc or BIC value. The function conducts a search over possible model within the order constraints provided. The parameters matches with the model.

Show the code

auto.arima((LLY_ts))Series: (LLY_ts)

ARIMA(0,1,0)

sigma^2 = 53.69: log likelihood = -11128.74

AIC=22259.49 AICc=22259.49 BIC=22265.58Step 5: Forecast

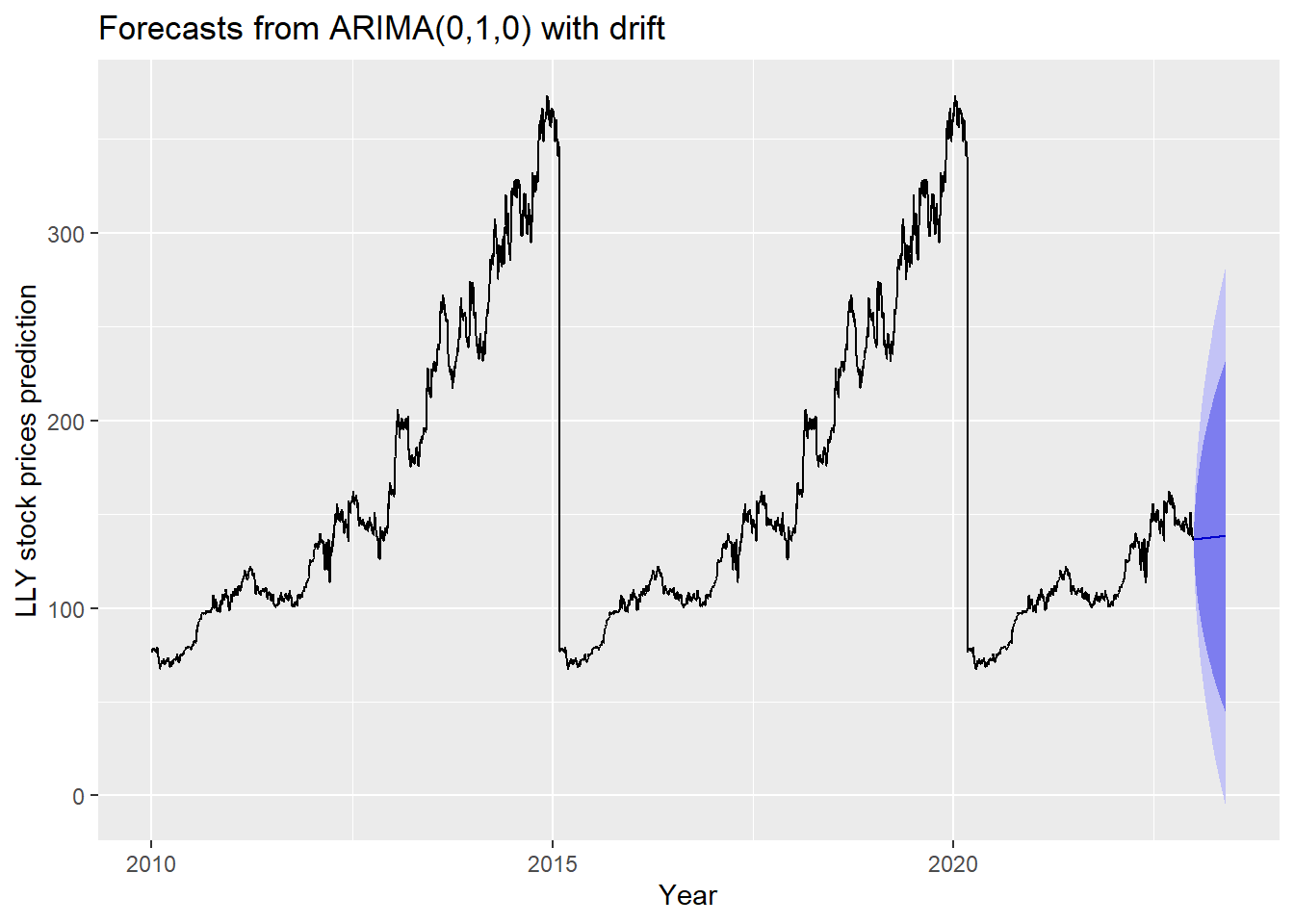

The blue part in graph below forecast the next 100 values of LLY stock price in 80% and 95% confidence level.

Show the code

LLY_ts %>%

Arima(order=c(0,1,0),include.drift = TRUE) %>%

forecast(100) %>%

autoplot() +

ylab("LLY stock prices prediction") + xlab("Year")

Step 6: Compare ARIMA model with the benchmark methods

Forecasting benchmarks are very important when testing new forecasting methods, to see how well they perform against some simple alternatives.

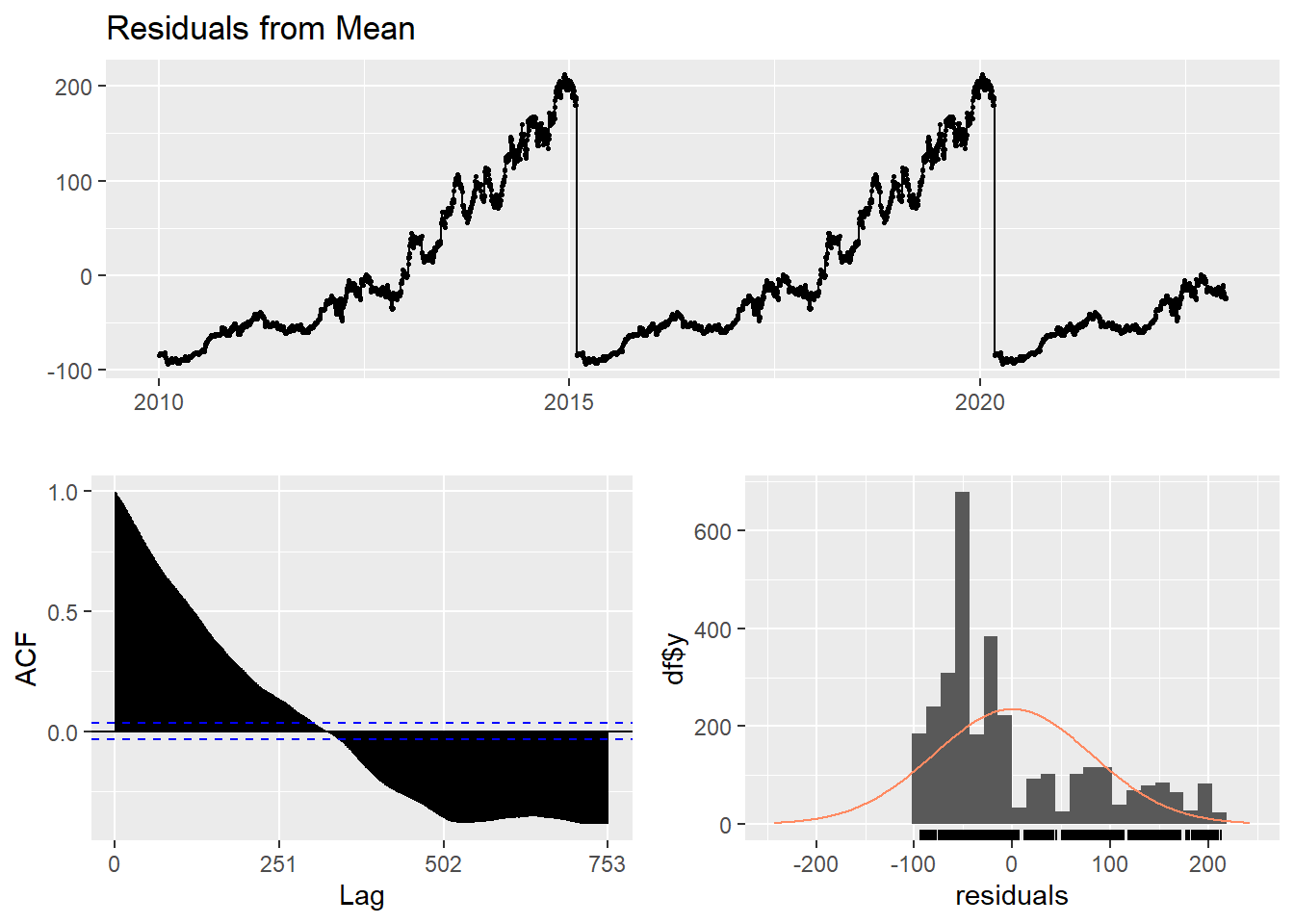

Average method

Here, the forecast of all future values are equal to the average of the historical data. The residual plot of this method is not stationary.

Show the code

f1<-meanf((LLY_ts), h=251) #mean

#summary(f1)

checkresiduals(f1)#serial correlation ; Lung Box p <0.05

Ljung-Box test

data: Residuals from Mean

Q* = 300420, df = 501, p-value < 2.2e-16

Model df: 1. Total lags used: 502Naive method

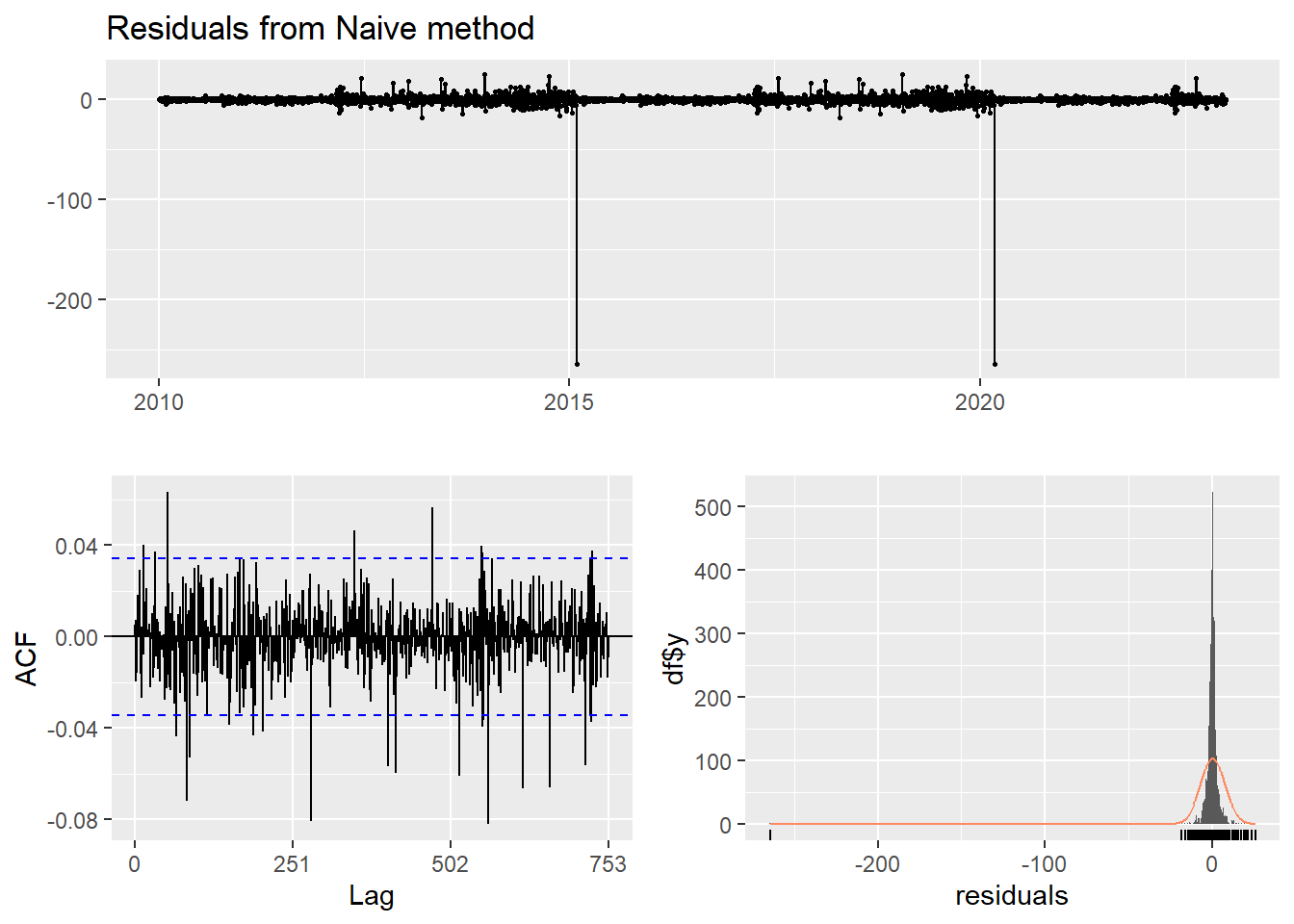

This method simply set all forecasts to be the value of the last observation. According to error measurement here, ARIMA(4,1,3) outperform the average method.

Show the code

f2<-naive((LLY_ts), h=11) # naive method

summary(f2)

Forecast method: Naive method

Model Information:

Call: naive(y = (LLY_ts), h = 11)

Residual sd: 7.3276

Error measures:

ME RMSE MAE MPE MAPE MASE

Training set 0.01834098 7.327602 2.208937 -0.1191376 1.444964 0.02769921

ACF1

Training set 0.004970975

Forecasts:

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2023.004 136.5567 127.1660 145.9474 122.19488 150.9186

2023.008 136.5567 123.2763 149.8372 116.24601 156.8674

2023.012 136.5567 120.2915 152.8219 111.68129 161.4321

2023.016 136.5567 117.7753 155.3381 107.83305 165.2804

2023.020 136.5567 115.5585 157.5550 104.44268 168.6708

2023.024 136.5567 113.5543 159.5591 101.37755 171.7359

2023.028 136.5567 111.7113 161.4022 98.55887 174.5546

2023.032 136.5567 109.9958 163.1176 95.93531 177.1781

2023.036 136.5567 108.3846 164.7288 93.47121 179.6422

2023.040 136.5567 106.8607 166.2527 91.14061 181.9728

2023.044 136.5567 105.4113 167.7021 88.92390 184.1895Show the code

checkresiduals(f2)#serial correlation ; Lung Box p <0.05

Ljung-Box test

data: Residuals from Naive method

Q* = 438.09, df = 502, p-value = 0.9816

Model df: 0. Total lags used: 502Seasonal naive method

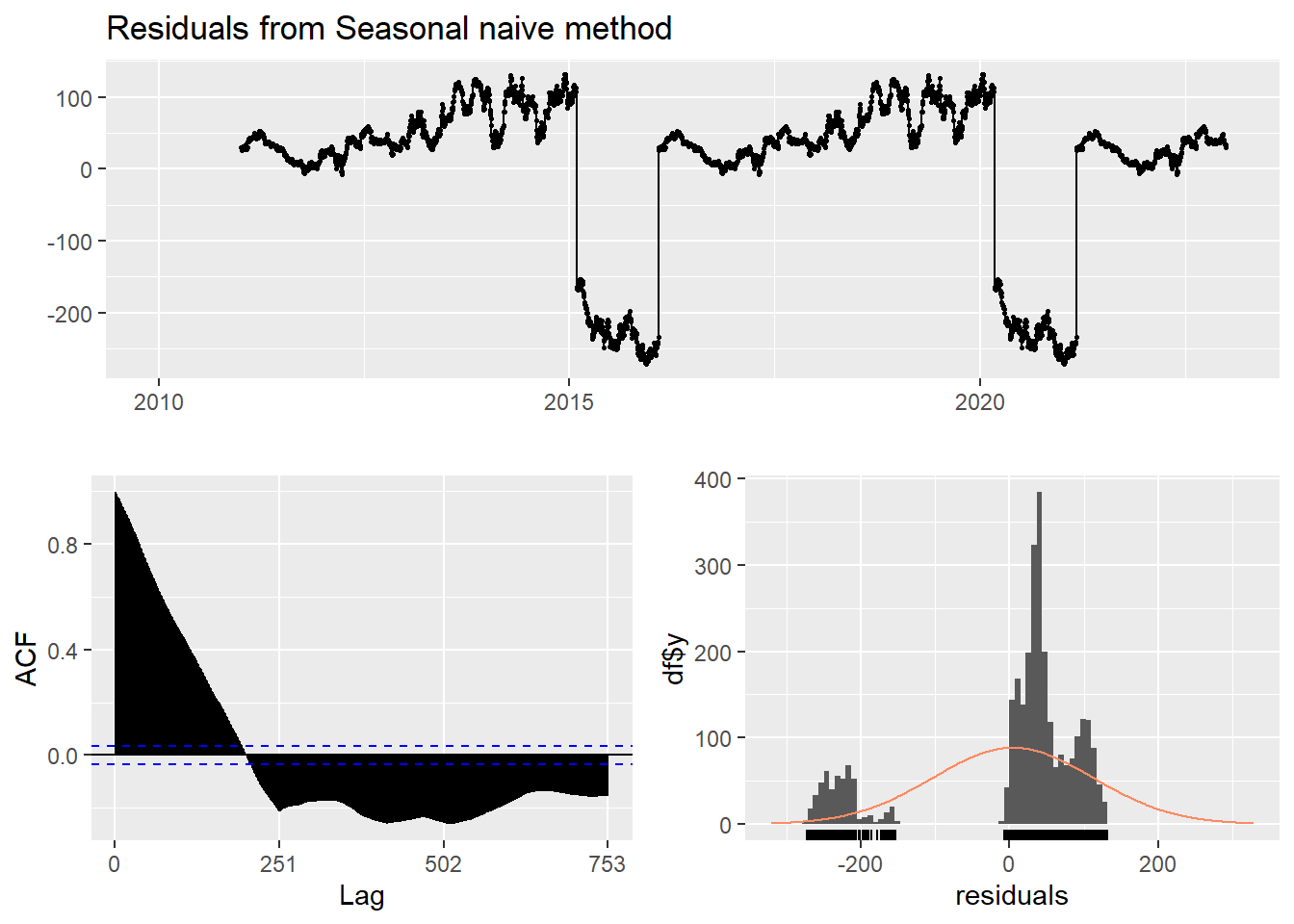

This method is useful for highly seasonal data, which can set each forecast to be equal to the last observed value from the same season of the year. Here seasonal naive is used to forecast the next 4 values for the LLY stock price series.

Show the code

f3<-snaive((LLY_ts), h=4) #seasonal naive method

summary(f3)

Forecast method: Seasonal naive method

Model Information:

Call: snaive(y = (LLY_ts), h = 4)

Residual sd: 108.2255

Error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 4.249799 108.2255 79.74729 -23.12158 65.75914 1 0.9950134

Forecasts:

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2023.004 105.4368 -33.25979 244.1334 -106.6813 317.5550

2023.008 106.4282 -32.26840 245.1248 -105.6899 318.5464

2023.012 107.5895 -31.10708 246.2861 -104.5286 319.7077

2023.016 106.2299 -32.46667 244.9265 -105.8882 318.3481Show the code

checkresiduals(f3) #serial correlation ; Lung Box p <0.05

Ljung-Box test

data: Residuals from Seasonal naive method

Q* = 235237, df = 502, p-value < 2.2e-16

Model df: 0. Total lags used: 502Drift Method

A variation on the naïve method is to allow the forecasts to increase or decrease over time, where the amount of change over time is set to be the average change seen in the historical data.

Show the code

f4 <- rwf((LLY_ts),drift=TRUE, h=20)

summary(f4)

Forecast method: Random walk with drift

Model Information:

Call: rwf(y = (LLY_ts), h = 20, drift = TRUE)

Drift: 0.0183 (se 0.1283)

Residual sd: 7.3287

Error measures:

ME RMSE MAE MPE MAPE MASE

Training set 5.431461e-15 7.327579 2.207391 -0.1331943 1.443601 0.02767983

ACF1

Training set 0.004970975

Forecasts:

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2023.004 136.5751 127.18151 145.9686 122.20887 150.9413

2023.008 136.5934 123.30688 149.8799 116.27342 156.9134

2023.012 136.6117 120.33665 152.8868 111.72114 161.5023

2023.016 136.6301 117.83435 155.4258 107.88449 165.3757

2023.020 136.6484 115.63094 157.6659 104.50496 168.7919

2023.024 136.6668 113.63975 159.6938 101.44998 171.8835

2023.028 136.6851 111.80928 161.5609 98.64081 174.7294

2023.032 136.7034 110.10600 163.3009 96.02617 177.3807

2023.036 136.7218 108.50663 164.9369 93.57042 179.8731

2023.040 136.7401 106.99419 166.4861 91.24765 182.2326

2023.044 136.7585 105.55590 167.9610 89.03826 184.4787

2023.048 136.7768 104.18182 169.3718 86.92707 186.6265

2023.052 136.7951 102.86403 170.7263 84.90198 188.6883

2023.056 136.8135 101.59613 172.0309 82.95318 190.6738

2023.060 136.8318 100.37284 173.2908 81.07261 192.5911

2023.064 136.8502 99.18974 174.5106 79.25351 194.4468

2023.068 136.8685 98.04311 175.6939 77.49018 196.2468

2023.072 136.8869 96.92975 176.8440 75.77774 197.9960

2023.076 136.9052 95.84692 177.9635 74.11198 199.6984

2023.080 136.9235 94.79222 179.0549 72.48925 201.3578Show the code

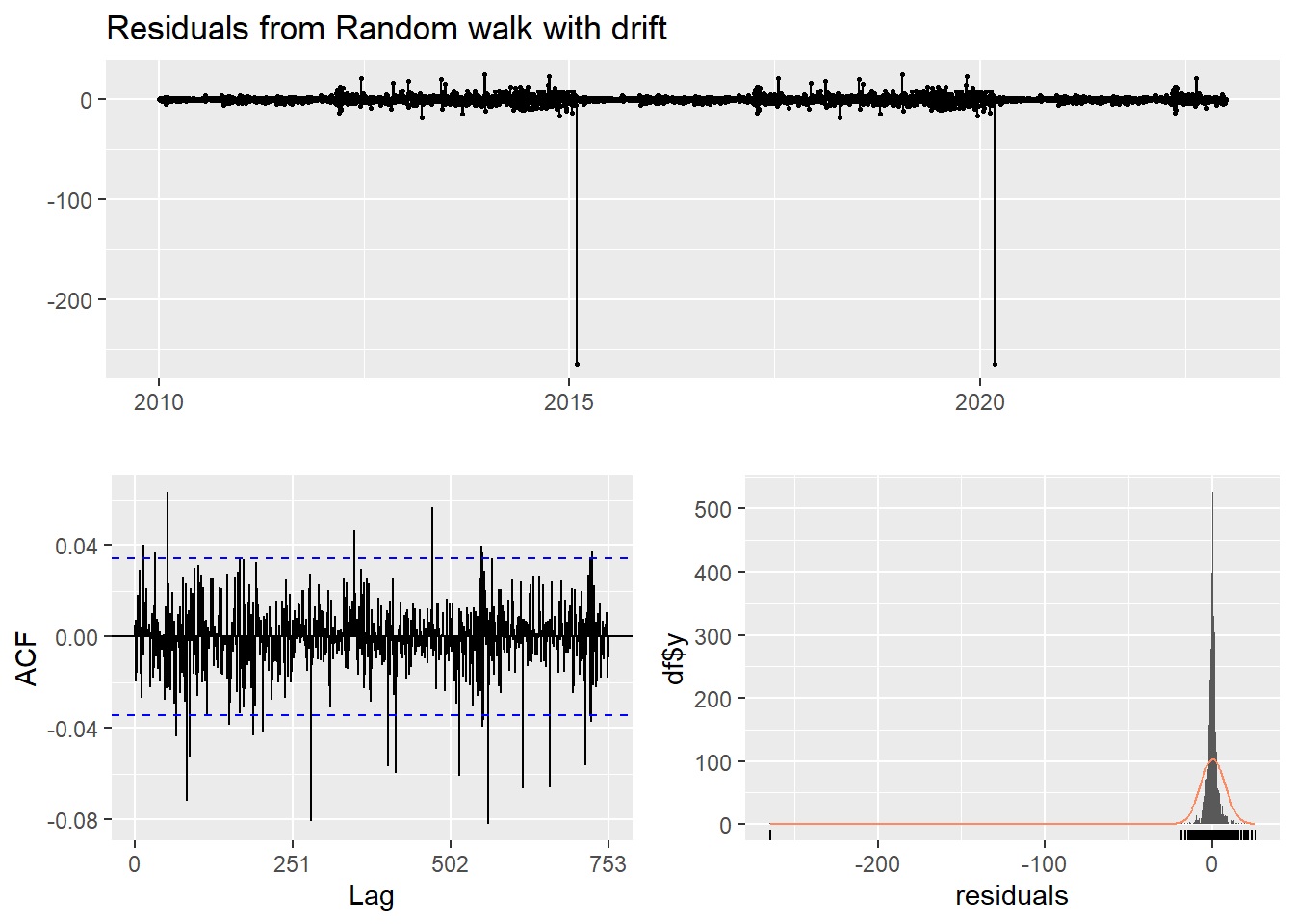

checkresiduals(f4)

Ljung-Box test

data: Residuals from Random walk with drift

Q* = 438.09, df = 501, p-value = 0.9801

Model df: 1. Total lags used: 502Show the code

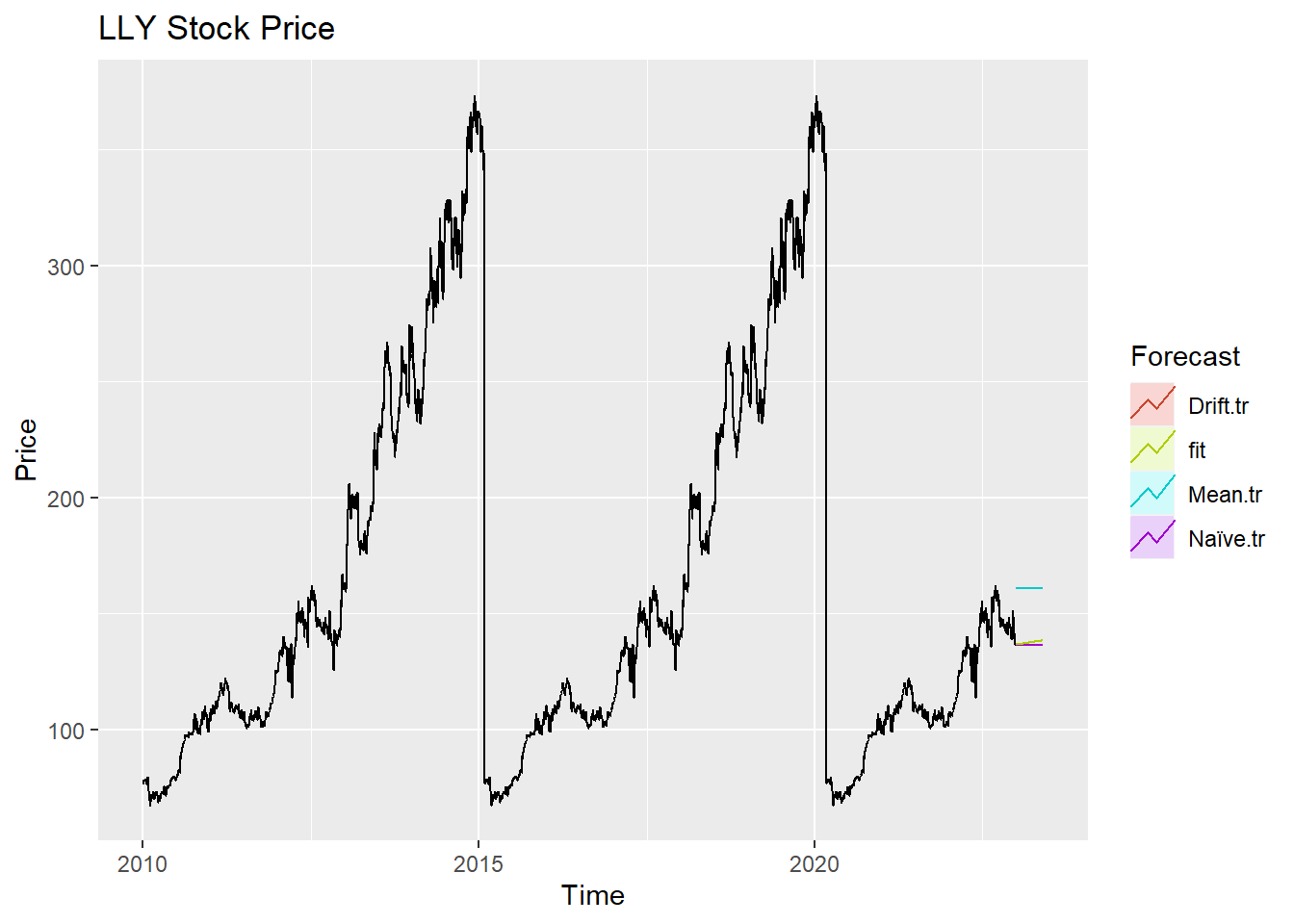

autoplot(LLY_ts) +

autolayer(meanf(LLY_ts, h=100),

series="Mean.tr", PI=FALSE) +

autolayer(naive((LLY_ts), h=100),

series="Naïve.tr", PI=FALSE) +

autolayer(rwf((LLY_ts), drift=TRUE, h=100),

series="Drift.tr", PI=FALSE) +

autolayer(forecast(fit1,100),

series="fit",PI=FALSE) +

ggtitle("LLY Stock Price") +

xlab("Time") + ylab("Price") +

guides(colour=guide_legend(title="Forecast"))

According to the graph above, ARIMA(0,1,0) outperform most of benchmark method, though its performance is very similar to drift method.