ARMA/ARIMA/SARIMA Models for UNH

Step 1: Determine the stationality of time series

Stationality is a pre-requirement of training ARIMA model. This is because term ‘Auto Regressive’ in ARIMA means it is a linear regression model that uses its own lags as predictors, which work best when the predictors are not correlated and are independent of each other. Stationary time series make sure the statistical properties of time series do not change over time.

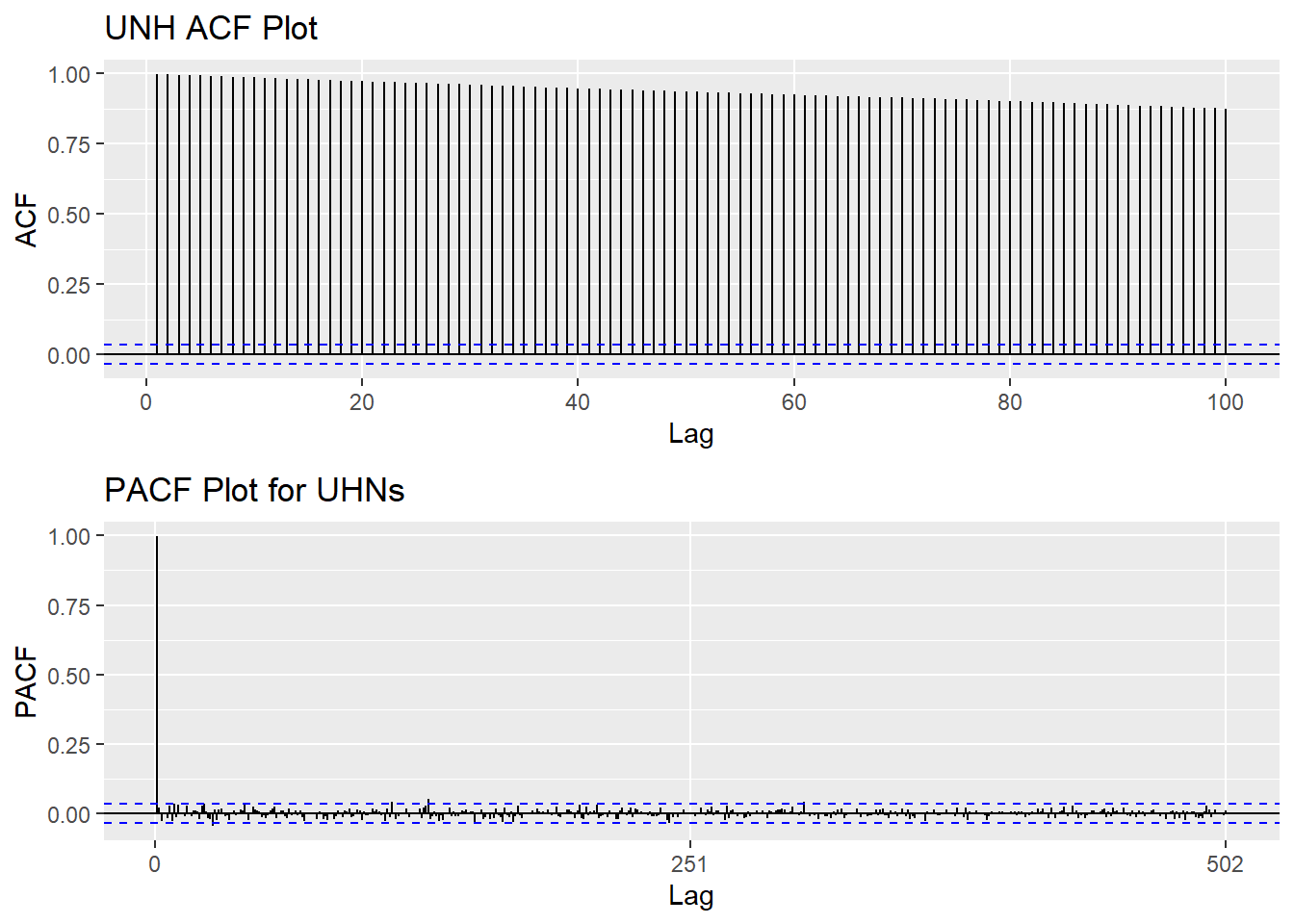

Based on information obtained from both ACF graphs and Augmented Dickey-Fuller Test, the time series data is non-stationary.

Show the code

UNH_acf <- ggAcf(UNH_ts,100)+ggtitle("UNH ACF Plot")

UNH_pacf <- ggPacf(UNH_ts)+ggtitle("PACF Plot for UHNs")

grid.arrange(UNH_acf, UNH_pacf,nrow=2)

Show the code

tseries::adf.test(UNH_ts)

Augmented Dickey-Fuller Test

data: UNH_ts

Dickey-Fuller = -1.0864, Lag order = 14, p-value = 0.9248

alternative hypothesis: stationaryStep 2: Eliminate Non-Stationality

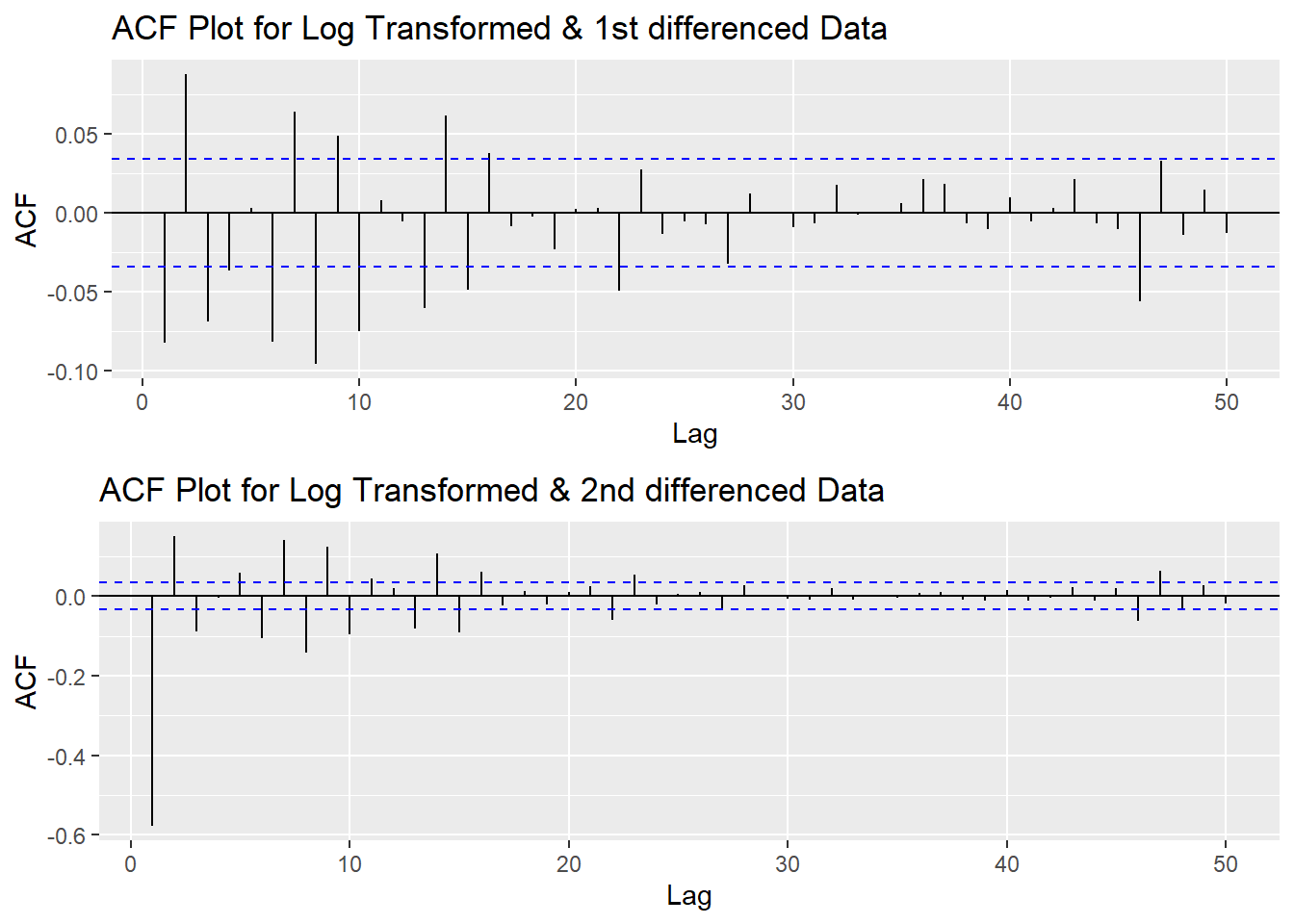

Since this data is non-stationary, it is important to necessary to convert it to stationary time series. This step employs a series of actions to eliminate non-stationality, i.e. log transformation and differencing the data. It turns out the log transformed and 1st differened data has shown good stationary property, there are no need to go further at 2nd differencing. What is more, the Augmented Dickey-Fuller Test also confirmed that the log transformed and 1st differenced data is stationary. Therefore, the log transformation and 1st differencing would be the actions taken to eliminate the non-stationality.

Show the code

plot1<- ggAcf(log(UNH_ts) %>%diff(), 50, main="ACF Plot for Log Transformed & 1st differenced Data")

plot2<- ggAcf(log(UNH_ts) %>%diff()%>%diff(),50, main="ACF Plot for Log Transformed & 2nd differenced Data")

grid.arrange(plot1, plot2,nrow=2)

Show the code

tseries::adf.test(log(UNH_ts) %>%diff())

Augmented Dickey-Fuller Test

data: log(UNH_ts) %>% diff()

Dickey-Fuller = -16.952, Lag order = 14, p-value = 0.01

alternative hypothesis: stationaryStep 3: Determine p,d,q Parameters

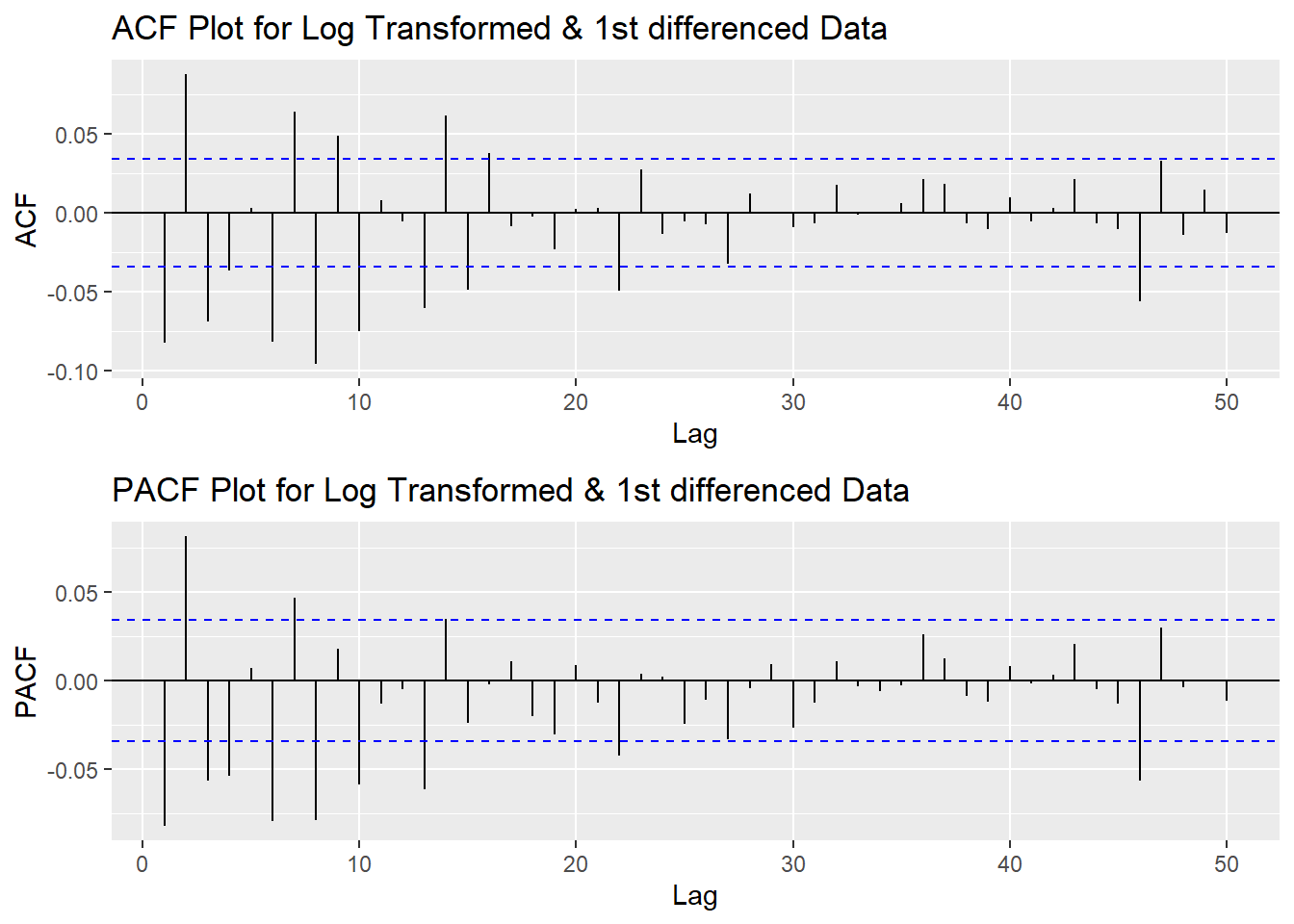

The standard notation of ARIMA(p,d,q) include p,d,q 3 parameters. Here are the representations: - p: The number of lag observations included in the model, also called the lag order; order of the AR term. - d: The number of times that the raw observations are differenced, also called the degree of differencing; number of differencing required to make the time series stationary. - q: order of moving average; order of the MA term. It refers to the number of lagged forecast errors that should go into the ARIMA Model.

Show the code

plot3<- ggPacf(log(UNH_ts) %>%diff(),50, main="PACF Plot for Log Transformed & 1st differenced Data")

grid.arrange(plot1,plot3)

According to the PACF plot and ACF plot above, here choose the range of p value and q value as 1-4 and 1-3, respectively. Since I only differenced the data once, the d would be 1.

Step 4: Fit ARIMA(p,d,q) model

Before fitting the data with ARIMA(p,d,q) model, we will need to choose the set of parameters based on error measurement and model diagnostics. Based on the result below, ARIMA(4,1,3) has lowest error measurement.

Show the code

################ Check for different combinations ######

d=1

i=1

temp= data.frame()

ls=matrix(rep(NA,6*12),nrow=12) # roughly nrow = 3x4x2

for (p in 2:5)# p=1,2,3,4 : 4

{

for(q in 2:4)# q=1,2,3 :3

{

for(d in 1:1)# d=1,2 :2

{

if(p-1+d+q-1<=8)

{

model<- Arima(log(UNH_ts),order=c(p-1,d,q-1),include.drift=TRUE)

ls[i,]= c(p-1,d,q-1,model$aic,model$bic,model$aicc)

i=i+1

#print(i)

}

}

}

}

temp= as.data.frame(ls)

names(temp)= c("p","d","q","AIC","BIC","AICc")

kable(temp) %>%

kable_styling(font_size = 12)| p | d | q | AIC | BIC | AICc |

|---|---|---|---|---|---|

| 1 | 1 | 1 | -17710.12 | -17685.76 | -17710.11 |

| 1 | 1 | 2 | -17719.11 | -17688.66 | -17719.09 |

| 1 | 1 | 3 | -17745.61 | -17709.07 | -17745.59 |

| 2 | 1 | 1 | -17716.76 | -17686.31 | -17716.74 |

| 2 | 1 | 2 | -17772.64 | -17736.10 | -17772.61 |

| 2 | 1 | 3 | -17747.50 | -17704.86 | -17747.46 |

| 3 | 1 | 1 | -17746.22 | -17709.68 | -17746.19 |

| 3 | 1 | 2 | -17745.07 | -17702.44 | -17745.04 |

| 3 | 1 | 3 | -17789.34 | -17740.62 | -17789.30 |

| 4 | 1 | 1 | -17728.60 | -17685.97 | -17728.56 |

| 4 | 1 | 2 | -17757.45 | -17708.73 | -17757.41 |

| 4 | 1 | 3 | -17798.95 | -17744.14 | -17798.90 |

Error measurement

Show the code

temp[which.min(temp$AIC),] p d q AIC BIC AICc

12 4 1 3 -17798.95 -17744.14 -17798.9 p d q AIC BIC AICc

12 4 1 3 -17798.95 -17744.14 -17798.9 p d q AIC BIC AICc

12 4 1 3 -17798.95 -17744.14 -17798.9Show the code

fit1 <- Arima(log(UNH_ts), order=c(4, 1, 3),include.drift = TRUE)

summary(fit1)Series: log(UNH_ts)

ARIMA(4,1,3) with drift

Coefficients:

ar1 ar2 ar3 ar4 ma1 ma2 ma3 drift

-0.6673 0.7666 0.7124 -0.0768 0.6040 -0.7506 -0.7104 9e-04

s.e. 0.0485 0.0455 0.0545 0.0218 0.0461 0.0382 0.0512 2e-04

sigma^2 = 0.0002496: log likelihood = 8908.48

AIC=-17798.95 AICc=-17798.9 BIC=-17744.14

Training set error measures:

ME RMSE MAE MPE MAPE

Training set 4.453197e-06 0.01577582 0.01103893 -0.0006003827 0.2395419

MASE ACF1

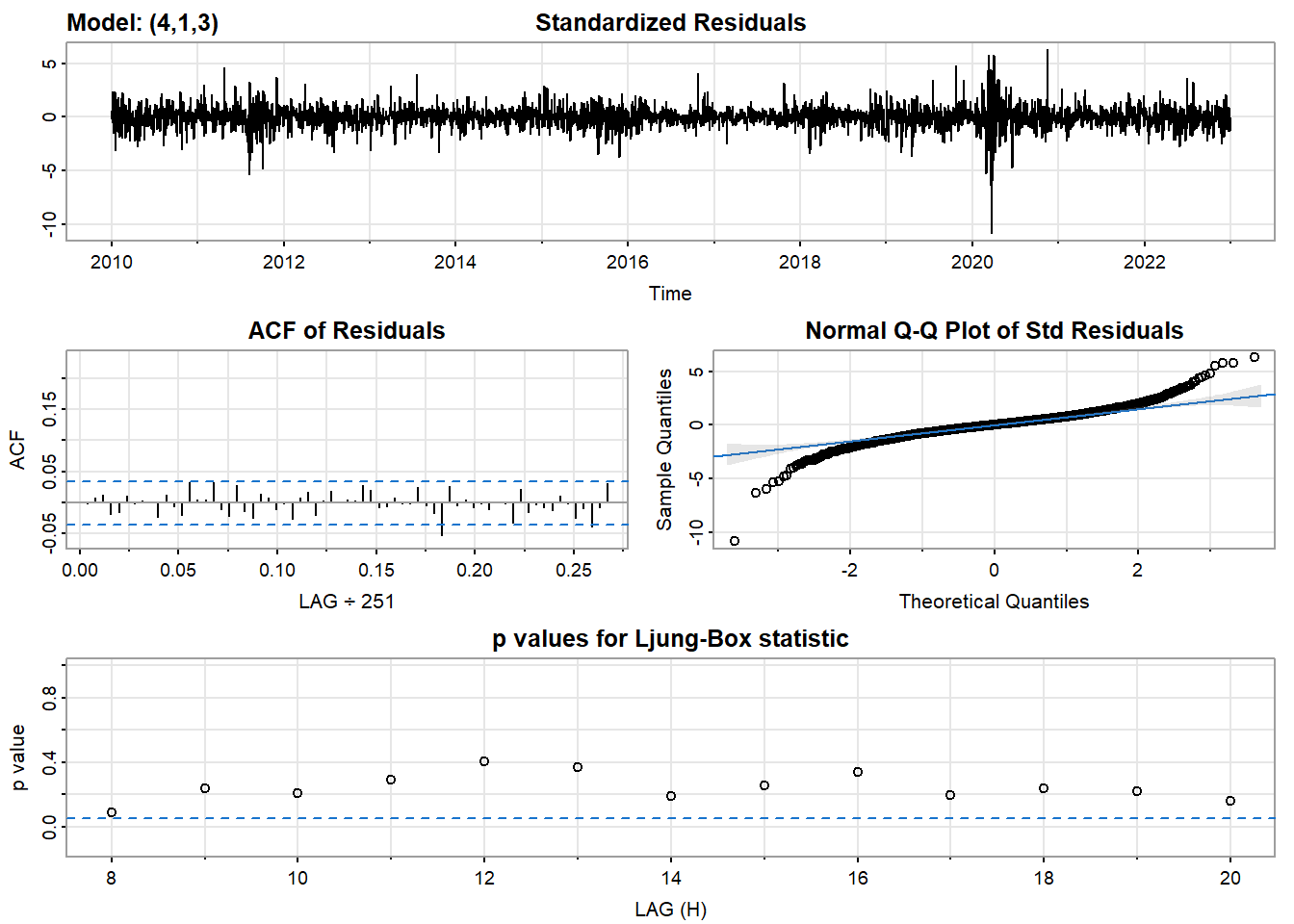

Training set 0.04432579 -0.0008705228Model Diagnostics

- Inspection of the time plot of the standardized residuals below shows no obvious patterns.

- Notice that there may be outliers, with a few values exceeding 3 standard deviations in magnitude.

- The ACF of the standardized residuals shows no apparent departure from the model assumptions, no significant lags shown.

- The normal Q-Q plot of the residuals shows that the assumption of normality is reasonable, with the exception of the fat-tailed.

- The model appears to fit well.

Show the code

model_output <- capture.output(sarima(log(UNH_ts), 4,1,3))

Show the code

cat(model_output[91:130], model_output[length(model_output)], sep = "\n") #to get rid of the convergence status and details of the optimization algorithm used by the sarima() final value -4.149087

converged

$fit

Call:

arima(x = xdata, order = c(p, d, q), seasonal = list(order = c(P, D, Q), period = S),

xreg = constant, transform.pars = trans, fixed = fixed, optim.control = list(trace = trc,

REPORT = 1, reltol = tol))

Coefficients:

ar1 ar2 ar3 ar4 ma1 ma2 ma3 constant

-0.6673 0.7666 0.7124 -0.0768 0.6040 -0.7506 -0.7104 9e-04

s.e. 0.0485 0.0455 0.0545 0.0218 0.0461 0.0382 0.0512 2e-04

sigma^2 estimated as 0.0002489: log likelihood = 8908.48, aic = -17798.95

$degrees_of_freedom

[1] 3255

$ttable

Estimate SE t.value p.value

ar1 -0.6673 0.0485 -13.7699 0e+00

ar2 0.7666 0.0455 16.8610 0e+00

ar3 0.7124 0.0545 13.0760 0e+00

ar4 -0.0768 0.0218 -3.5325 4e-04

ma1 0.6040 0.0461 13.1042 0e+00

ma2 -0.7506 0.0382 -19.6542 0e+00

ma3 -0.7104 0.0512 -13.8675 0e+00

constant 0.0009 0.0002 6.1278 0e+00

$AIC

[1] -5.454781

$AICc

[1] -5.454768

$BIC

[1] -5.437983

NACompare with auto.arima() function

auto.arima() returns best ARIMA model according to either AIC, AICc or BIC value. The function conducts a search over possible model within the order constraints provided. However, this method is not reliable sometimes. It fits a different model than ACF/PACF plots suggest. This is because auto.arima() usually return models that are more complex as it prefers more parameters compared than to the for example BIC.

Show the code

auto.arima(log(UNH_ts))Series: log(UNH_ts)

ARIMA(1,1,0) with drift

Coefficients:

ar1 drift

-0.0821 9e-04

s.e. 0.0174 3e-04

sigma^2 = 0.0002582: log likelihood = 8850.38

AIC=-17694.76 AICc=-17694.76 BIC=-17676.49Step 5: Forecast

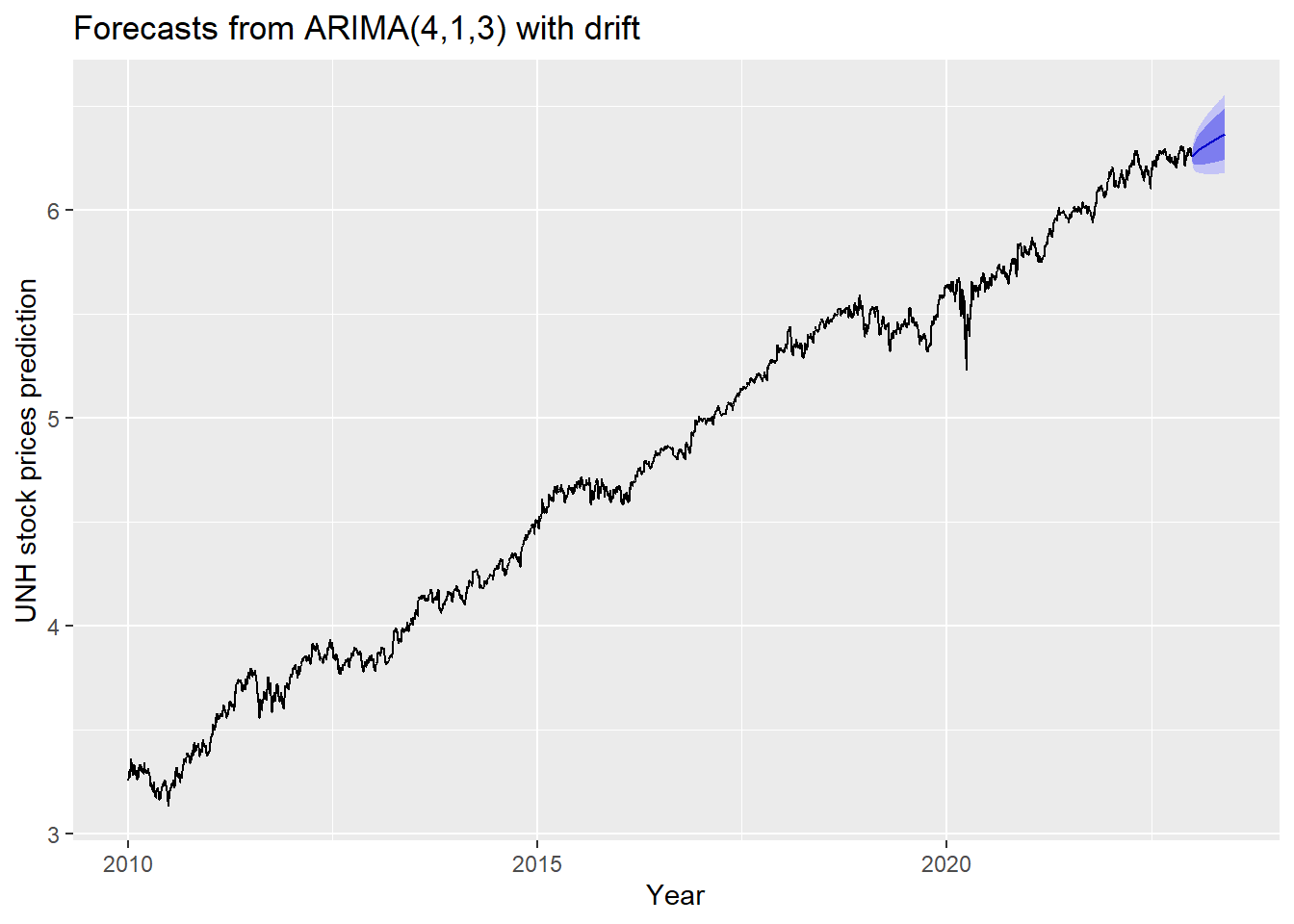

The blue part in graph below forecast the next 100 values of UNH stock price in 80% and 95% confidence level.

Show the code

log(UNH_ts) %>%

Arima(order=c(4,1,3),include.drift = TRUE) %>%

forecast(100) %>%

autoplot() +

ylab("UNH stock prices prediction") + xlab("Year")

Step 6: Compare ARIMA model with the benchmark methods

Forecasting benchmarks are very important when testing new forecasting methods, to see how well they perform against some simple alternatives.

Average method

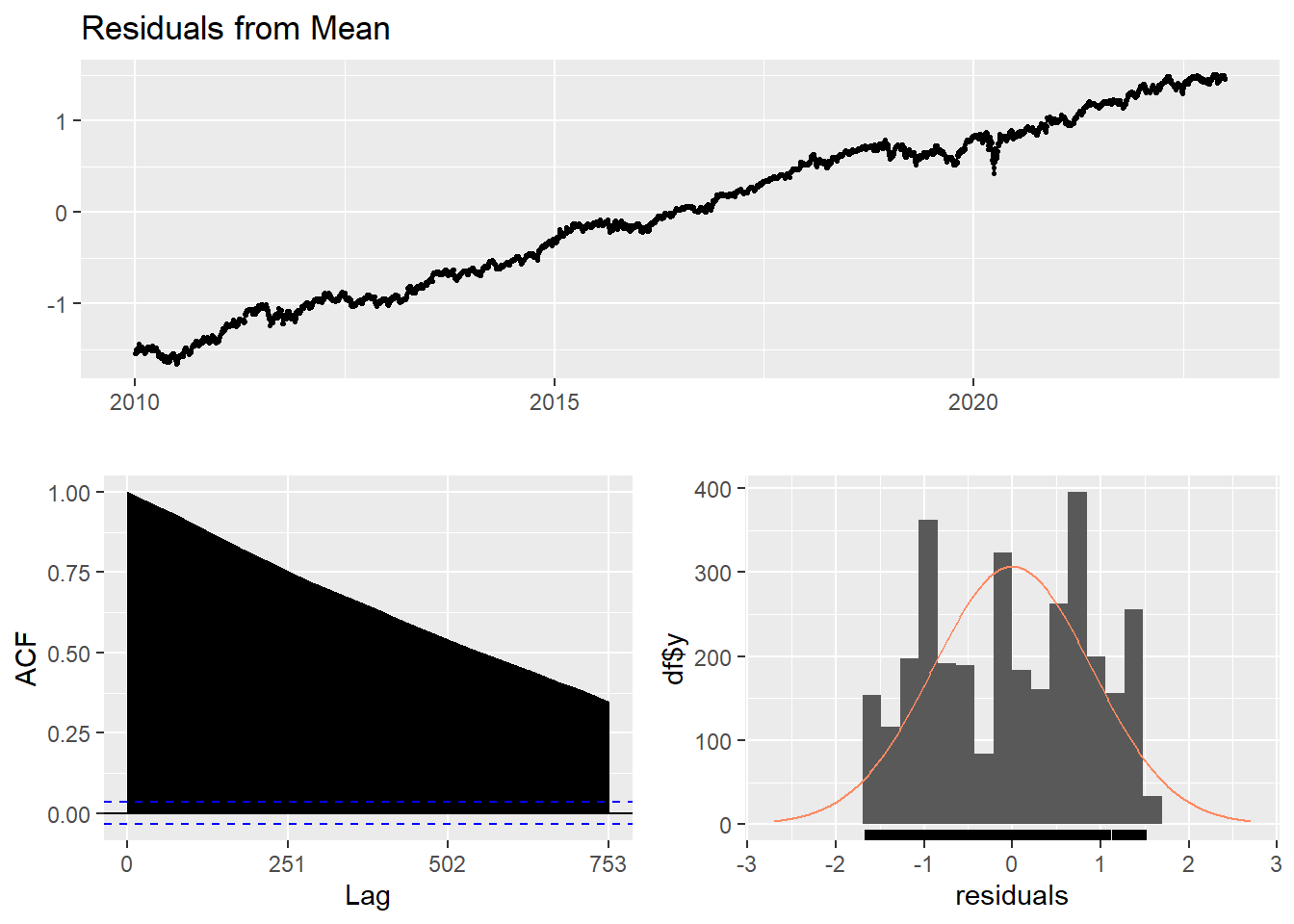

Here, the forecast of all future values are equal to the average of the historical data. The residual plot of this method is not stationary.

Show the code

f1<-meanf(log(UNH_ts), h=251) #mean

#summary(f1)

checkresiduals(f1)#serial correlation ; Lung Box p <0.05

Ljung-Box test

data: Residuals from Mean

Q* = 1046300, df = 501, p-value < 2.2e-16

Model df: 1. Total lags used: 502Naive method

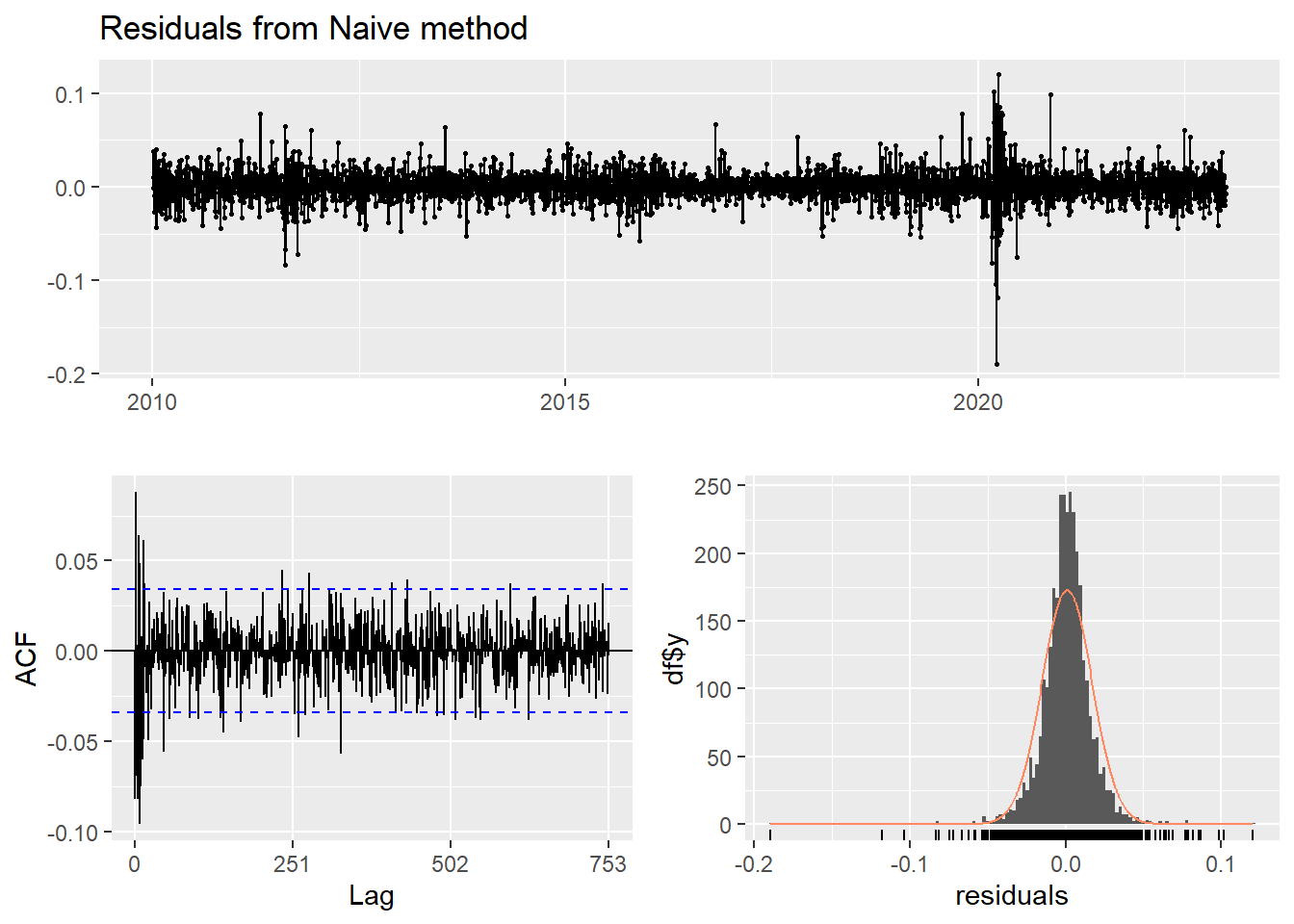

This method simply set all forecasts to be the value of the last observation. According to error measurement here, ARIMA(4,1,3) outperform the average method.

Show the code

f2<-naive(log(UNH_ts), h=11) # naive method

summary(f2)

Forecast method: Naive method

Model Information:

Call: naive(y = log(UNH_ts), h = 11)

Residual sd: 0.0161

Error measures:

ME RMSE MAE MPE MAPE MASE

Training set 0.0009204042 0.01614298 0.01110733 0.01941981 0.2408094 0.04460044

ACF1

Training set -0.08216434

Forecasts:

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2023.004 6.257173 6.236484 6.277861 6.225533 6.288812

2023.008 6.257173 6.227915 6.286430 6.212427 6.301918

2023.012 6.257173 6.221340 6.293005 6.202371 6.311974

2023.016 6.257173 6.215796 6.298549 6.193893 6.320452

2023.020 6.257173 6.210913 6.303432 6.186424 6.327921

2023.024 6.257173 6.206497 6.307848 6.179671 6.334674

2023.028 6.257173 6.202437 6.311908 6.173462 6.340883

2023.032 6.257173 6.198658 6.315687 6.167682 6.346663

2023.036 6.257173 6.195108 6.319237 6.162254 6.352092

2023.040 6.257173 6.191751 6.322594 6.157119 6.357226

2023.044 6.257173 6.188558 6.325787 6.152236 6.362109Show the code

checkresiduals(f2)#serial correlation ; Lung Box p <0.05

Ljung-Box test

data: Residuals from Naive method

Q* = 685.37, df = 502, p-value = 8.794e-08

Model df: 0. Total lags used: 502Seasonal naive method

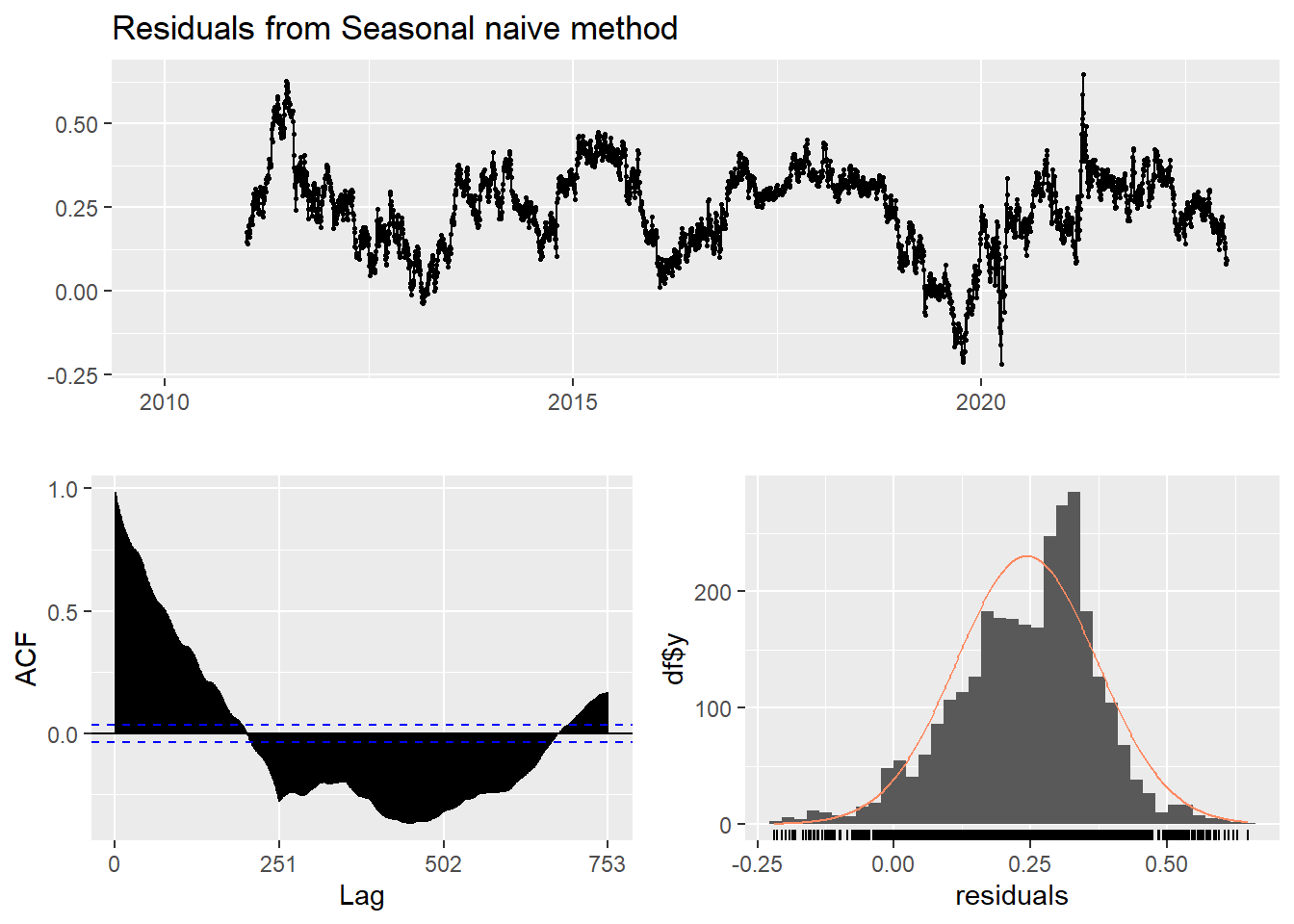

This method is useful for highly seasonal data, which can set each forecast to be equal to the last observed value from the same season of the year. Here seasonal naive is used to forecast the next 4 values for the UNH stock price series.

Show the code

f3<-snaive(log(UNH_ts), h=4) #seasonal naive method

summary(f3)

Forecast method: Seasonal naive method

Model Information:

Call: snaive(y = log(UNH_ts), h = 4)

Residual sd: 0.2754

Error measures:

ME RMSE MAE MPE MAPE MASE ACF1

Training set 0.2432513 0.2753742 0.2490408 5.098921 5.207824 1 0.9842087

Forecasts:

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2023.004 6.172414 5.819508 6.525321 5.632691 6.712138

2023.008 6.186518 5.833612 6.539424 5.646794 6.726241

2023.012 6.189044 5.836138 6.541951 5.649321 6.728768

2023.016 6.197327 5.844421 6.550233 5.657603 6.737050Show the code

checkresiduals(f3) #serial correlation ; Lung Box p <0.05

Ljung-Box test

data: Residuals from Seasonal naive method

Q* = 226574, df = 502, p-value < 2.2e-16

Model df: 0. Total lags used: 502Drift Method

A variation on the naïve method is to allow the forecasts to increase or decrease over time, where the amount of change over time is set to be the average change seen in the historical data.

Show the code

f4 <- rwf(log(UNH_ts),drift=TRUE, h=20)

summary(f4)

Forecast method: Random walk with drift

Model Information:

Call: rwf(y = log(UNH_ts), h = 20, drift = TRUE)

Drift: 9e-04 (se 3e-04)

Residual sd: 0.0161

Error measures:

ME RMSE MAE MPE MAPE

Training set 1.071097e-16 0.01611672 0.0110743 -0.0004837745 0.2401268

MASE ACF1

Training set 0.04446783 -0.08216434

Forecasts:

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2023.004 6.258093 6.237432 6.278754 6.226495 6.289691

2023.008 6.259013 6.229790 6.288237 6.214320 6.303706

2023.012 6.259934 6.224137 6.295730 6.205188 6.314680

2023.016 6.260854 6.219514 6.302195 6.197629 6.324079

2023.020 6.261775 6.215547 6.308002 6.191076 6.332473

2023.024 6.262695 6.212048 6.313342 6.185237 6.340153

2023.028 6.263615 6.208902 6.318329 6.179938 6.347292

2023.032 6.264536 6.206036 6.323036 6.175068 6.354004

2023.036 6.265456 6.203398 6.327514 6.170546 6.360366

2023.040 6.266377 6.200952 6.331802 6.166318 6.366435

2023.044 6.267297 6.198668 6.335926 6.162338 6.372256

2023.048 6.268217 6.196526 6.339909 6.158575 6.377860

2023.052 6.269138 6.194508 6.343768 6.155001 6.383275

2023.056 6.270058 6.192599 6.347517 6.151595 6.388522

2023.060 6.270979 6.190788 6.351169 6.148338 6.393619

2023.064 6.271899 6.189066 6.354732 6.145217 6.398581

2023.068 6.272819 6.187424 6.358214 6.142219 6.403420

2023.072 6.273740 6.185856 6.361624 6.139333 6.408147

2023.076 6.274660 6.184354 6.364966 6.136549 6.412771

2023.080 6.275581 6.182914 6.368247 6.133860 6.417301Show the code

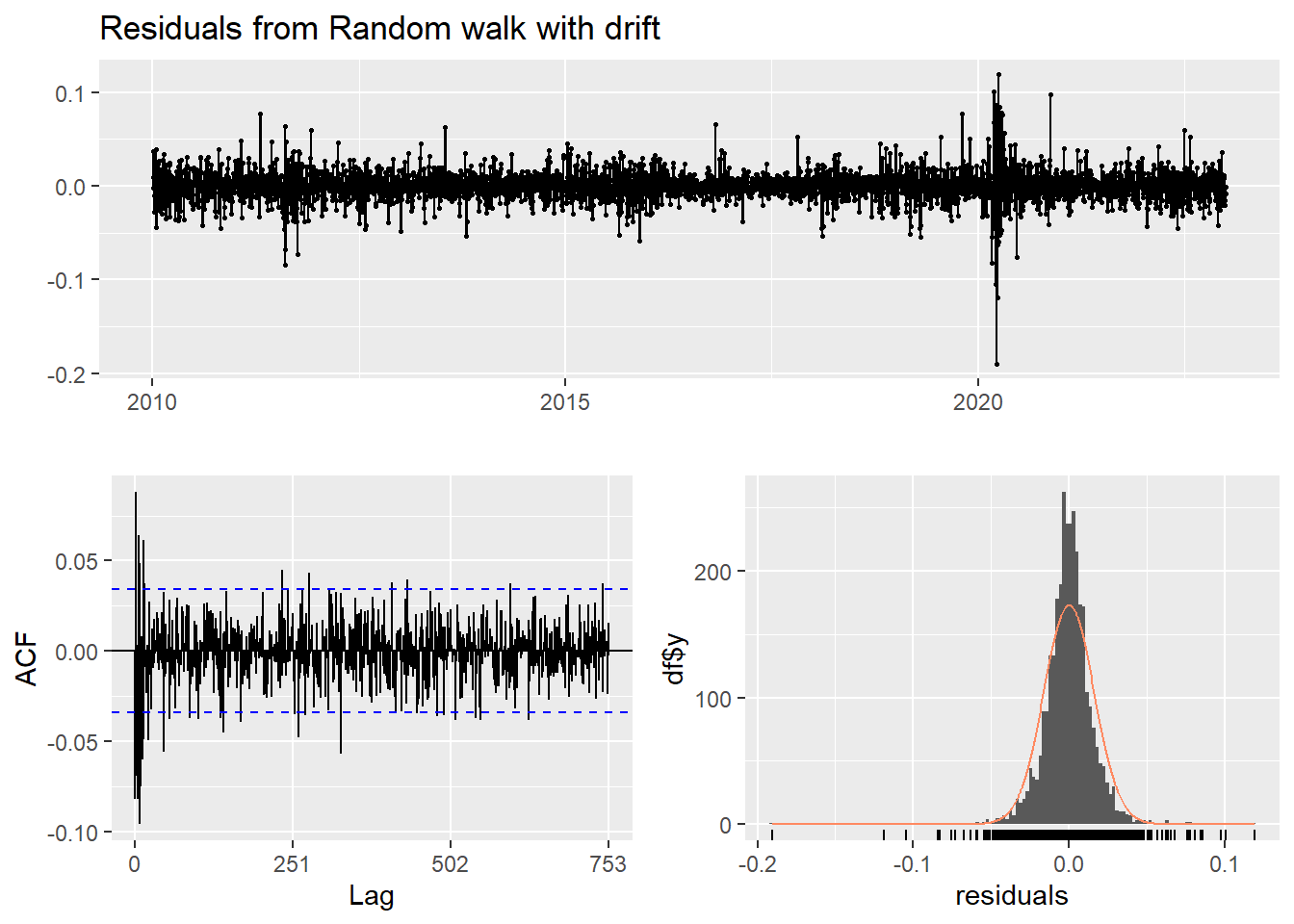

checkresiduals(f4)

Ljung-Box test

data: Residuals from Random walk with drift

Q* = 685.37, df = 501, p-value = 7.477e-08

Model df: 1. Total lags used: 502Show the code

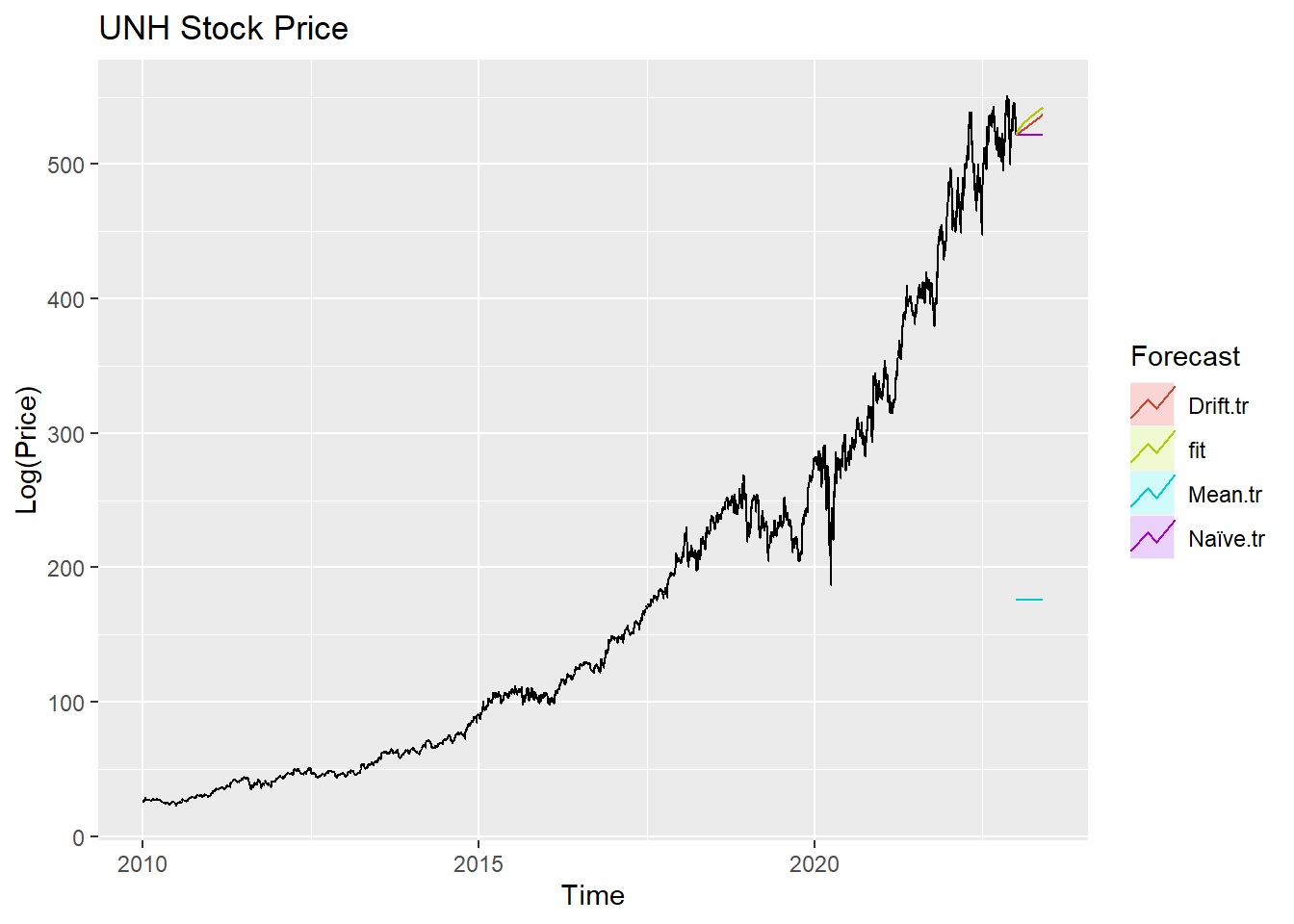

autoplot(UNH_ts) +

autolayer(meanf(UNH_ts, h=100),

series="Mean.tr", PI=FALSE) +

autolayer(naive((UNH_ts), h=100),

series="Naïve.tr", PI=FALSE) +

autolayer(rwf((UNH_ts), drift=TRUE, h=100),

series="Drift.tr", PI=FALSE) +

autolayer(forecast(Arima((UNH_ts), order=c(4, 1, 3),include.drift = TRUE),100),

series="fit",PI=FALSE) +

ggtitle("UNH Stock Price") +

xlab("Time") + ylab("Log(Price)") +

guides(colour=guide_legend(title="Forecast"))

According to the graph above, ARIMA(4,1,3) outperform most of benchmark method, though its performance is very similar to drift method.